How lenders evaluate business health is a process of combining financial ratio analysis with qualitative assessments to determine a company’s creditworthiness and repayment capacity. Lenders do not simply scan a profit and loss statement. They apply a structured framework covering cash flow sufficiency, leverage, liquidity, management quality, and market conditions. The 5 Cs of credit (Character, Capacity, Capital, Collateral, and Conditions) form the backbone of this process. Small business owners who understand this framework apply with stronger documentation, better financial positioning, and a far higher chance of approval.

Lenders start with numbers. The specific ratios they calculate reveal whether a business can service new debt without straining operations.

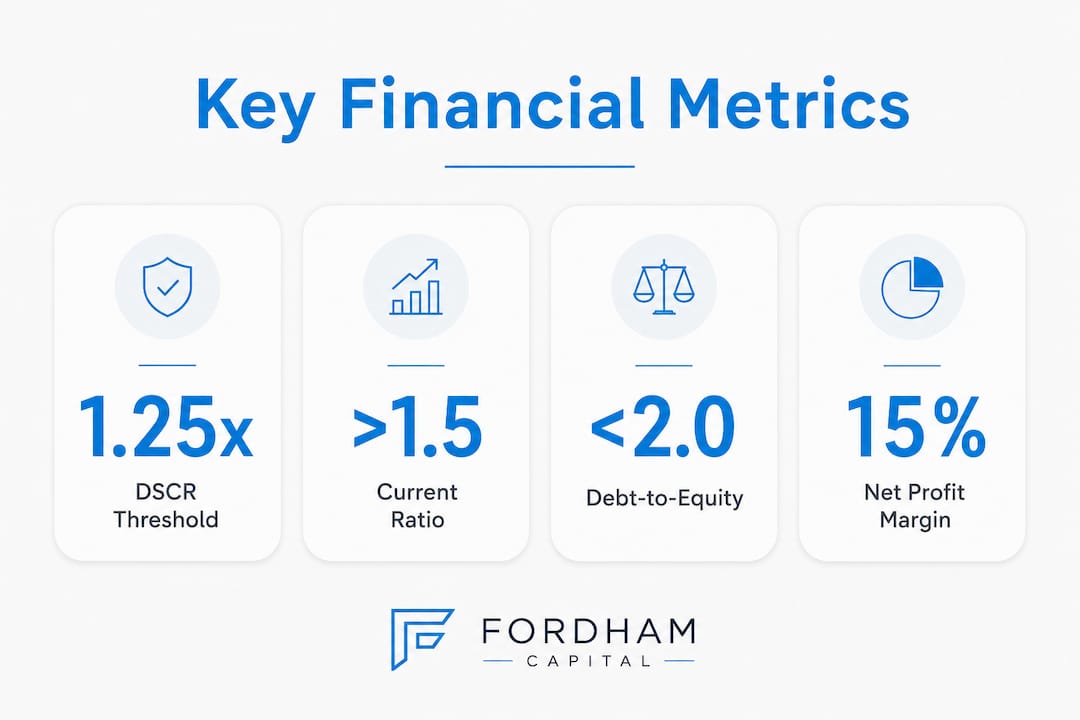

The Debt Service Coverage Ratio (DSCR) is the single most important metric in commercial lending. DSCR measures net operating income divided by total debt obligations. Most lenders require a minimum of 1.25x, meaning the business generates $1.25 in operating income for every $1.00 of debt payment due. A DSCR below 1.0x signals the business cannot cover its debt from operations alone.

Liquidity ratios tell lenders how quickly a business can meet short-term obligations. The current ratio (current assets divided by current liabilities) and the quick ratio (which strips out inventory) both indicate financial flexibility. A current ratio below 1.0 is a red flag in most industries.

Leverage ratios measure how much of the business is funded by debt versus owner equity. The debt-to-equity ratio and debt-to-worth ratio both appear in standard commercial credit analysis. High leverage signals that a business is already stretched, which raises the lender’s risk exposure on any new loan.

Profitability ratios round out the picture. Net profit margin and gross margin show whether the business model itself generates sustainable returns. A business with strong revenue but thin margins may still fail the DSCR test if operating costs consume most of that income.

| Ratio | What it measures | Typical lender benchmark |

|---|---|---|

| DSCR | Ability to repay debt from operations | Minimum 1.25x |

| Current ratio | Short-term liquidity | Above 1.0 |

| Debt-to-equity | Financial leverage | Lower is better; varies by industry |

| Net profit margin | Profitability efficiency | Positive and trending upward |

| Quick ratio | Immediate liquidity without inventory | Above 0.8 |

Lenders also benchmark these ratios against industry peers using resources like the RMA Annual Statement Studies. A ratio that looks weak in isolation may be average for a specific sector. Trend analysis over 2–3 years accompanies every ratio review, because trajectory matters as much as the current snapshot.

Pro Tip: Never assume a profitable business automatically qualifies for a loan. Lenders weight cash flow timing and DSCR coverage far more than accounting profit. A business can show net income on paper while failing the DSCR test due to large depreciation add-backs or deferred liabilities.

Qualitative factors determine the outcome of borderline loan decisions. Management strength and market conditions often tip the scales when financial ratios sit near the approval threshold.

The 5 Cs framework structures how lenders assess these softer elements:

Management quality receives serious scrutiny. Lenders assess whether the leadership team has the operational experience to execute the business plan. A business with strong financials but a first-time owner in a complex industry faces harder questions than one led by a 10-year veteran.

Customer concentration risk is another factor that directly affects lender evaluation criteria. When more than 25–30% of revenue comes from a single client, lenders treat that as a structural vulnerability. Losing one customer could collapse cash flow overnight.

Pro Tip: Prepare a one-page management summary for your loan application. List each key team member’s relevant experience, their role, and any industry credentials. Lenders read this before the financials. A credible team narrative reduces perceived risk before a single number is reviewed.

Early-stage lenders apply a different lens. Without years of financial history, they focus on signals that predict future repayment ability rather than past performance.

Startups are assessed on their path to profitability, recurring revenue models, and growth metrics like month-over-month revenue increases. Predictable recurring revenue, such as subscription contracts or retainer agreements, carries far more weight than one-time project income. Lenders want to see that revenue will still exist when the first loan payment comes due.

Runway and burn rate matter for venture-style debt. Lenders typically want to see 12–18 months of runway and a burn rate below 20–30% of monthly recurring revenue. These thresholds signal that the business has enough time to reach profitability without requiring emergency refinancing.

Personal credit fills the gap where business history is absent. Startups rely heavily on the owner’s personal credit score, personal income, and personal cash reserves when the company lacks its own track record. Personal guarantees and collateral are standard requirements for early-stage loans.

Investor backing also signals credibility. A startup that has raised equity from institutional investors demonstrates that experienced parties have already vetted the business model. Lenders treat that as third-party validation.

Key documents early-stage lenders typically require include:

For founders navigating this process, startup funding options vary significantly by lender type, and matching the right lender to your stage matters as much as the application itself.

Preparation before applying is the single biggest lever a business owner controls. Lenders reward businesses that arrive organized, financially sound, and transparent.

Build cash reserves. A healthy business maintains cash covering 3–6 months of fixed operating expenses. Less than 3 months of reserves signals vulnerability to lenders and increases the probability of a declined application.

Diversify your customer base. Revenue concentration above 25% from one client is a penalized risk factor. Actively reducing dependence on any single customer improves both your business resilience and your lender score.

Normalize your financial statements. Lenders perform a process called “spreading,” which standardizes your financials for comparison against industry benchmarks. Prepare clean, consistent statements for the past 2–3 years. Remove one-time items and owner perks that distort true operating performance.

Improve your DSCR before applying. Pay down existing debt, reduce discretionary expenses, or increase revenue to push your DSCR above 1.25x. Even a modest improvement from 1.1x to 1.3x can move an application from declined to approved.

Write a clear use-of-funds statement. Lenders want to know exactly where the money goes and how it generates returns. A vague answer raises doubt. A specific plan (for example, purchasing equipment that reduces production costs by a defined amount) builds confidence.

Check your personal credit. For small businesses, personal credit directly affects loan eligibility. Resolve any errors on your credit report and pay down personal revolving balances before applying.

Understanding what lenders look for in a complete application saves time and prevents the frustration of a declined submission.

Lenders approve loans based on a combination of financial ratios, qualitative factors, and business trajectory, not profit alone.

| Point | Details |

|---|---|

| DSCR is the top metric | Lenders require a minimum 1.25x DSCR to approve most commercial loans. |

| Qualitative factors decide close calls | Management quality and customer concentration often determine borderline decisions. |

| Startups need personal credit | Early-stage businesses rely on owner credit, guarantees, and runway data in place of financial history. |

| Cash reserves signal stability | Maintaining 3–6 months of operating expenses in reserve reduces lender-perceived risk. |

| Normalize financials before applying | Clean, standardized statements aligned to lender benchmarks improve approval odds significantly. |

Most business owners walk into a loan application believing their revenue number is the headline. Lenders do not see it that way. Revenue is just the top line. What matters is what survives after every expense, debt payment, and owner draw is accounted for.

I have seen businesses with $3 million in annual revenue get declined because their DSCR sat at 0.9x. The money was coming in, but it was leaving just as fast. Conversely, I have seen a $400,000-revenue business with a 1.6x DSCR and a seasoned owner get approved quickly, because every number told a coherent story of control and capacity.

The other mistake I see constantly is treating the loan application as a transaction rather than a conversation. Lenders are assessing trust. A business owner who can explain their financials, articulate their growth plan, and acknowledge their risks honestly is far more credible than one who presents polished numbers but stumbles on basic questions.

In 2026, lenders are also paying closer attention to revenue quality, not just revenue volume. Recurring, contracted income scores higher than project-based or seasonal income. If your business has both, separate them clearly in your presentation. Show the lender exactly how much of your revenue is predictable.

The owners who get funded are not always the ones with the best numbers. They are the ones who understand what the lender needs to feel confident, and then deliver exactly that.

— Rob

Small business owners who understand lender evaluation criteria are already ahead of most applicants. The next step is finding a lender who matches that preparation with a process that does not waste your time.

Fordhamcapital works with small and medium-sized businesses that traditional banks often overlook. With a one-page application, no credit impact during the review process, and approvals within 24 hours, Fordhamcapital removes the friction that slows most funding decisions. The company holds an A+ BBB rating and has funded over $120M, helping clients generate more than $500M in revenue. Whether your business is established or early-stage, you can apply for funding and get a decision without the delays that come with conventional lending.

Most commercial lenders require a Debt Service Coverage Ratio of at least 1.25x. This means the business must generate $1.25 in net operating income for every $1.00 of debt payment due.

Lenders assess startups on recurring revenue, month-over-month growth, runway length, and the owner’s personal credit. Collateral and personal guarantees are standard requirements when business history is limited.

Revenue concentration above 25–30% from a single client is treated as a risk factor by lenders. Diversifying your customer base before applying reduces this penalty and strengthens your overall credit profile.

Lenders normalize, or “spread,” financial statements to remove one-time items and owner adjustments that distort true operating performance. This allows them to compare your business against industry benchmarks on a consistent basis.

Yes. A business can show net profit on its income statement while failing the DSCR test due to high debt obligations or poor cash flow timing. Lenders weight repayment capacity over accounting profit in every credit decision.

At Fordham Capital, we've made the application process straightforward and reassuring. Dive in and explore your financial options with confidence, knowing there's no impact on your credit score and no obligations. We review your details and offer customized solutions based on what you're looking for.