Collateral free loans are business financing products that require no pledge of assets such as property, equipment, or inventory, making them the fastest route to capital for most small and medium enterprises. Known in the lending industry as unsecured business loans, these products have become the default choice for SMEs that need funding quickly without putting hard-won assets on the line. Digital-first lenders like Fordham Capital have cut approval times to 24 hours or less, a pace that traditional bank secured loans cannot match. For business owners who need to move fast on inventory, expansion, or an unexpected expense, that speed is the whole argument.

The core reason unsecured business loans work so well for SMEs comes down to one word: access. Most small businesses do not own commercial real estate or expensive machinery free and clear, so a secured loan is simply not an option. Collateral free financing removes that barrier entirely, shifting the lender’s focus from what you own to how your business performs.

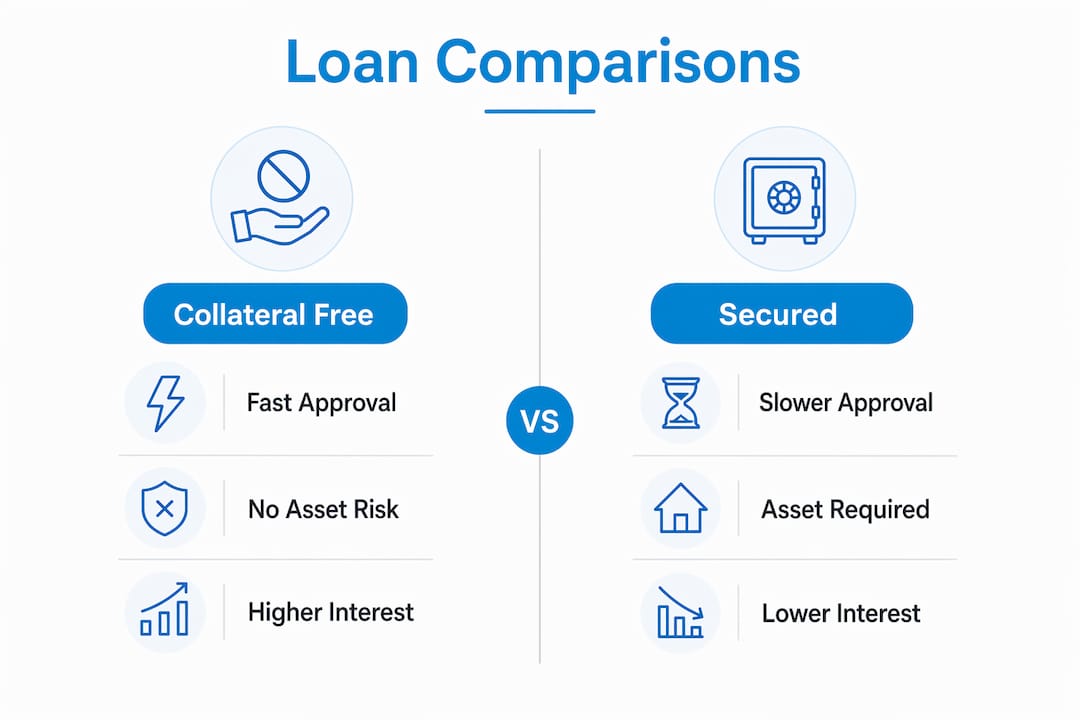

Here is what makes these loans a natural fit for SME needs:

The practical use cases are broad. A retailer can fund a holiday inventory build. A service firm can cover payroll during a slow quarter. A startup can finance equipment upgrades without waiting for a secured loan approval that may never come.

Pro Tip: Before applying, map out exactly what the loan will fund and calculate the expected return. If a $50,000 inventory purchase generates $80,000 in revenue within the repayment window, the higher interest rate on an unsecured loan is a cost worth paying.

Lenders replace the security of collateral with the security of financial performance. That means eligibility criteria are specific and non-negotiable. Understanding them before you apply saves time and protects your credit.

Government-backed programs add another layer. Schemes like the CGTMSE in India cover 75% to 90% of lender risk through guarantee coverage, which is why qualifying businesses can access better rates. The trade-off is compliance complexity, including specific revenue caps and sector eligibility rules.

If your credit score is below 700, explore options designed for that profile. Fordham Capital’s guide on funding with low credit scores outlines eight real alternatives that do not require a perfect credit history.

The choice between unsecured and secured financing is not about which product is better. It is about which one matches your current position and your immediate need.

| Factor | Collateral free loans | Secured loans |

|---|---|---|

| Approval speed | 24 to 48 hours with digital lenders | 2 to 6 weeks for traditional banks |

| Interest rate | 14% to 22% per year | 7% to 12% per year (asset-backed) |

| Loan amount | Typically lower, based on cash flow | Higher, based on asset value |

| Asset risk | No specific asset pledged | Asset seized on default |

| Personal liability | Often requires personal guarantee | Tied to pledged collateral |

| Best for | Speed, flexibility, no asset ownership | Large capital needs, lower cost priority |

The interest rate gap is real. Higher rates on unsecured products reflect the lender’s increased risk, and that cost gets passed directly to the borrower. For a $100,000 loan, the difference between 10% and 18% annual interest is roughly $8,000 per year. That is a meaningful number.

The counterargument is opportunity cost. A secured loan that takes six weeks to approve may cause you to miss a contract, a supplier deal, or a market window that was worth far more than $8,000. Strategic use of unsecured loans can outweigh the higher interest cost when the business move it enables creates lasting value.

Pro Tip: Run a simple break-even calculation before choosing. Divide the extra annual interest cost by the expected monthly revenue gain from the funded activity. If the payback period is under six months, the unsecured loan almost always wins on a net basis.

For businesses that need to understand the risk profile of faster financing in more detail, Fordham Capital’s breakdown of high-risk business loans explains how lenders price and manage credit risk across different loan types.

Getting approved is step one. Using the loan well is the part that actually determines whether it helps or hurts your business.

A working capital loan is one of the most common and effective applications for collateral free financing. It covers the gap between when you pay suppliers and when customers pay you, without requiring you to pledge the inventory itself as security.

Collateral free loans suit businesses because they deliver fast capital without asset risk, making them the most practical funding tool for SMEs that need to move quickly and preserve operational flexibility.

| Point | Details |

|---|---|

| No asset pledge required | Businesses keep property and equipment free of lender claims throughout the loan term. |

| Approval in 24 to 48 hours | Digital lenders like Fordham Capital approve and disburse funds far faster than traditional banks. |

| Credit score drives eligibility | A score of 700 or above unlocks the most competitive rates, typically 14% to 22% per year. |

| Personal guarantees still apply | Most collateral free loans include a personal guarantee, creating real personal liability on default. |

| Strategic use maximizes value | Funding inventory, expansion, or working capital generates returns that offset the higher interest cost. |

Most business owners approach unsecured loans with one of two wrong assumptions. Either they treat them as a last resort because the rates are higher, or they treat them as free money because nothing is pledged. Both views cost money.

The rate difference between a secured and unsecured loan is a real cost, but it is a fixed, calculable cost. What is not calculable is the value of the opportunity you miss while waiting six weeks for a secured loan to process. I have seen businesses lose supplier relationships, miss seasonal windows, and watch competitors take market share, all because they were waiting on a bank that required an appraisal of assets they barely owned. The businesses that used collateral free financing moved faster and came out ahead, even after paying the higher rate.

The personal guarantee issue is where I see the most dangerous blind spots. Business owners hear “collateral free” and assume they have no personal exposure. That is wrong in most cases. Read the guarantee clause before you sign. Know what triggers it and what it covers. That one paragraph in the loan agreement matters more than the interest rate.

The smartest use of these loans I have observed is as a bridge to better financing. A business takes an unsecured loan, uses it well, builds its credit profile, and qualifies for a larger secured facility at a lower rate 18 months later. The first loan is not the destination. It is the credential.

— Rob

Fordham Capital was built specifically for businesses that cannot afford to wait weeks for a funding decision. The one-page application connects you to a network of banks and lenders, with approvals delivered within 24 hours and no credit impact from the inquiry. Fordham has funded over $120M for SMEs and helped clients generate more than $500M in revenue, backed by an A+ BBB rating. If you need fast business funding without pledging assets, Fordham Capital is the place to start. The process is direct, the terms are transparent, and the funding is real.

A collateral free business loan, also called an unsecured business loan, provides capital without requiring the borrower to pledge property, equipment, or other assets as security. Lenders evaluate creditworthiness, revenue history, and business performance instead.

Digital lenders approve and disburse collateral free loans in as little as 24 to 48 hours, compared to two to six weeks for traditional secured bank loans.

Yes, in most cases. Many unsecured loans include a personal guarantee that holds the business owner personally liable for repayment, even though no specific asset is formally pledged.

Most lenders require a credit score of 700 or above to qualify for competitive rates. Scores below that threshold may still qualify but typically result in higher interest rates within the 14% to 22% annual range.

Defaulting damages your credit score and can lead to legal action, including wage garnishment, even without collateral. The lender’s recourse shifts from seizing assets to pursuing legal and credit remedies.

At Fordham Capital, we've made the application process straightforward and reassuring. Dive in and explore your financial options with confidence, knowing there's no impact on your credit score and no obligations. We review your details and offer customized solutions based on what you're looking for.