A business term loan is a lump sum of capital borrowed from a lender and repaid with interest over a fixed period, typically ranging from 3 months to 25 years. This structure gives you predictable monthly payments, a defined payoff date, and a clear cost of capital before you sign. Whether you’re buying equipment, funding an expansion, or covering a one-time operational expense, a term loan is one of the most widely used financing tools available to small and medium-sized businesses. Lenders including U.S. Bank, the SBA, and a broad network of private lenders all offer term loan products with varying rates, terms, and qualification requirements.

A business term loan is disbursed as a single lump sum directly into your business account once approved. You then repay that amount plus interest through regular installments, typically monthly, over the agreed loan term. Unlike a revolving credit line, the funds are deposited once and the repayment schedule is fixed from day one.

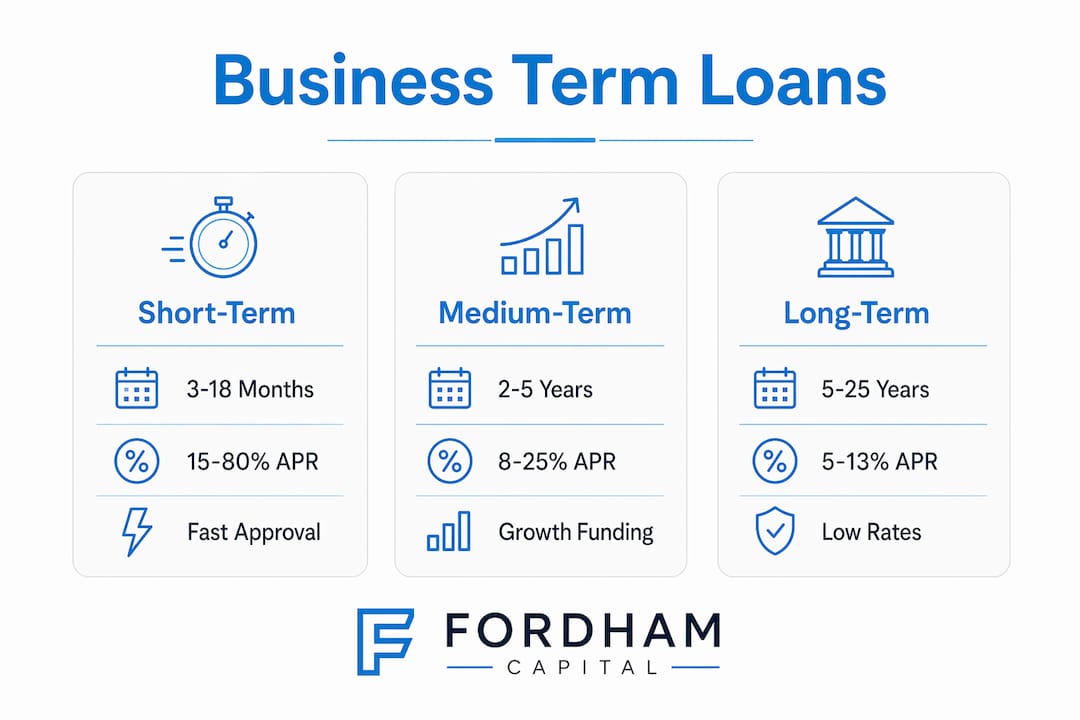

Loan terms span a wide range. Short-term loans run 3 to 18 months, medium-term loans cover 2 to 5 years, and long-term loans can extend up to 25 years for capital-intensive investments like commercial real estate. The term you choose directly shapes two numbers that matter most: your monthly payment and your total interest cost.

Term length affects cost in a straightforward but often underestimated way. A shorter term means higher monthly payments but less total interest paid over the life of the loan. A longer term lowers your monthly obligation but increases the total amount you pay back. This tradeoff is not just math. It reflects how much cash flow pressure you can absorb each month versus how much you’re willing to pay for breathing room.

Most term loans use an amortization schedule, meaning each payment covers both principal and interest. In the early months, a larger share of each payment goes toward interest rather than reducing the principal balance. This is a critical detail if you ever plan to pay off the loan early, because your remaining balance may be higher than you expect.

Pro Tip: Ask any lender for a full amortization table before signing. Run the numbers for month 6, month 12, and the midpoint of your loan. You’ll see exactly how much principal you’ve actually paid down at any point.

Interest rates on term loans vary significantly by loan type. Short-term loans carry 15 to 80% APR, medium-term loans range from 7 to 30%, and long-term loans from established lenders typically fall between 5 and 13% APR. The rate you receive depends on your credit profile, time in business, revenue, and the lender’s risk appetite.

Three distinct categories of business term loans exist, each built for different business situations, risk profiles, and funding timelines.

Short-term loans run 3 to 18 months and are the most commonly approved financing type for small businesses. Speed drives their popularity: many owners prioritize fast access to capital over lower interest rates when facing urgent operational needs. Approval can happen within 24 to 48 hours, and credit score requirements are lower, often starting at 500. The tradeoff is cost. APRs can reach 80%, making short-term loans expensive if used for anything other than a high-return, near-term opportunity.

Medium-term loans cover 2 to 5 years and represent the middle ground most growing businesses actually need. Rates are more manageable at 7 to 30% APR, funding amounts are higher, and lenders typically require a credit score of 600 or above with at least two years in business. These loans work well for equipment purchases, hiring campaigns, or marketing investments with a clear return horizon.

Long-term loans extend from 5 to 25 years and carry the lowest interest rates, typically 5 to 13% APR. SBA loans fall into this category, as do commercial real estate loans from banks like U.S. Bank and Wells Fargo. Qualification is stricter, with most lenders preferring credit scores of 650 or higher, strong financials, and often collateral. The benefit is a lower monthly payment spread over a long runway, which preserves cash flow for operations.

| Loan type | Typical term | APR range | Best use case | Min. credit score |

|---|---|---|---|---|

| Short-term | 3 to 18 months | 15 to 80% | Urgent cash needs, inventory | 500+ |

| Medium-term | 2 to 5 years | 7 to 30% | Equipment, hiring, marketing | 600+ |

| Long-term | 5 to 25 years | 5 to 13% | Real estate, major expansion | 650+ |

Pro Tip: If your credit score sits below 600, explore low credit funding options before applying for a long-term loan. A rejection can delay your timeline and affect your borrowing options.

A term loan is also structurally different from a working capital loan or a revolving line of credit. Term loans suit planned, one-time expenditures rather than ongoing or unpredictable operational costs. If your funding need is recurring or variable, a line of credit is likely the better tool.

Choosing the right term loan is less about finding the lowest rate and more about matching the loan structure to your specific business situation. Follow this sequence before you apply.

Define the purpose of the funds. A piece of equipment with a 7-year useful life should not be financed with an 18-month loan. Mismatching loan term to asset life is one of the most common and costly mistakes business owners make. Short-term loans for long-term assets create cash flow strain. Long-term loans for short-term needs generate unnecessary interest expense.

Analyze your monthly cash flow. Pull your last 12 months of bank statements and identify your lowest revenue month. Your loan payment must be serviceable in that worst-case month, not just your average month. If the payment strains your slowest period, the term is too short or the loan amount is too large.

Calculate the total cost, not just the rate. A 9% APR on a 5-year loan costs more in total interest than a 15% APR on a 12-month loan for the same principal. Run both scenarios with an amortization calculator before comparing offers.

Match lender type to your profile. SBA lenders and traditional banks offer the best rates but require strong credit and documentation. Online lenders and alternative finance companies move faster and accept lower credit scores, but at higher rates. Know which category you qualify for before spending time on applications.

Consider the collateral requirement. Many term loans, especially long-term ones, require collateral or a personal guarantee. If you prefer to avoid pledging assets, look into collateral-free loan options before committing to a secured structure.

Matching loan maturity to cash flow cycles is the single most important factor in avoiding repayment stress. Businesses that get this right treat debt as a precision tool rather than a lifeline.

Several factors in term loan agreements catch business owners off guard after signing. Understanding them upfront protects both your cash flow and your personal finances.

Amortization front-loads interest. Early payments cover mostly interest, not principal. If you plan to refinance or sell the business within the first half of the loan term, your payoff balance will be higher than you likely expect. Request a full amortization schedule and review it before signing.

Personal guarantees are common and binding. Collateral in small business loans frequently includes a personal guarantee, meaning you are personally liable if the business defaults. This is not a formality. Clarify the exact terms of any guarantee before you sign, including whether it is limited or unlimited in scope.

Watch for origination fees and prepayment penalties. Some lenders charge 1 to 5% of the loan amount as an origination fee, which reduces your effective proceeds. Others charge prepayment penalties if you pay off the loan early. Both affect your true cost of capital and should be factored into any comparison.

Pre-approval protects your credit. Many lenders offer soft-pull pre-approvals that do not affect your credit score. Use these to compare offers before submitting a formal application, which typically triggers a hard inquiry.

Pro Tip: If a lender cannot clearly explain their fee structure in writing before you apply, treat that as a signal to look elsewhere. Transparent lenders document everything upfront.

Understanding personal guarantee requirements early in the process gives you time to negotiate terms or explore alternatives before you’re committed.

A business term loan works best when the loan term, repayment amount, and purpose are aligned with your business’s cash flow and asset life.

| Point | Details |

|---|---|

| Definition | A term loan delivers a lump sum repaid with interest over a fixed period of 3 months to 25 years. |

| Rate by term | Short-term APRs reach 80%; long-term loans from established lenders typically run 5 to 13%. |

| Match term to asset | Finance assets for no longer than their useful life to avoid cash flow strain or excess interest. |

| Personal guarantees | Many small business term loans require personal liability; clarify scope before signing. |

| Amortization impact | Early payments are interest-heavy; your payoff balance mid-loan is higher than most owners expect. |

I’ve seen business owners treat a term loan approval as the finish line when it’s actually the starting line. The real work begins after the funds hit your account.

The most common mistake I observe is borrowing based on the maximum approved amount rather than the minimum needed. Lenders approve you for what you qualify for, not what’s optimal for your business. Taking $300,000 because you were approved for it, when $180,000 would cover the actual need, means paying interest on $120,000 that’s sitting idle or being spent on lower-priority items.

The second pattern I see repeatedly is ignoring the amortization schedule until it’s too late. A business owner refinances at month 18 of a 5-year loan, expecting to have paid down a significant chunk of principal, and discovers the balance is barely lower than when they started. That’s not a lender trick. It’s math. But it’s math that most people don’t look at until they’re already in the deal.

My honest advice: before you sign any term loan, build a simple spreadsheet with three columns. Month, remaining balance, and cumulative interest paid. Run it to the end of the loan. Then run it to the point where you might want to exit or refinance. That exercise will tell you more about whether the loan is right for your business than any rate comparison will.

Term loans are genuinely useful tools. They fund real growth. But they reward business owners who treat them with the same rigor they’d apply to hiring a key employee or signing a major contract.

— Rob

Fordham Capital works with small and medium-sized businesses that need fast, flexible financing without the friction of traditional bank lending. Their one-page application connects you to a wide network of banks and lenders, with approvals available within 24 hours and no credit impact from the initial inquiry.

With an A+ BBB rating and over $120M funded, Fordham Capital has helped business owners access the capital they need to grow on their own terms. Whether you’re evaluating a term loan, exploring alternatives, or simply want to understand your options before committing, their team provides transparent, personalized guidance from the first conversation. Visit Fordham Capital to explore your funding options today.

The loan term is the length of time you have to repay the borrowed amount in full, including interest. Terms range from 3 months for short-term loans to 25 years for long-term commercial financing.

A term loan is a specific type of business loan defined by its lump-sum disbursement and fixed repayment schedule. Other business loan types include lines of credit, invoice financing, and merchant cash advances, each with different structures and repayment mechanics.

Short-term loans often accept scores of 500 or above, while long-term loans from banks and SBA lenders typically require 650 or higher. Stronger credit scores unlock lower rates and longer terms.

Approval timelines vary by lender type. Online and alternative lenders can approve and fund within 24 to 48 hours. Traditional banks and SBA lenders typically take 2 to 8 weeks due to more extensive underwriting requirements.

Term loans are better suited for planned, one-time expenses like equipment or expansion. Lines of credit fit ongoing or unpredictable costs better because you draw and repay funds as needed rather than receiving a fixed lump sum.

At Fordham Capital, we've made the application process straightforward and reassuring. Dive in and explore your financial options with confidence, knowing there's no impact on your credit score and no obligations. We review your details and offer customized solutions based on what you're looking for.