A business plan is the primary document lenders use to decide whether your business can reliably repay a loan. It is not a marketing brochure or a vision statement. Lenders treat it as a risk assessment tool, and the role of business plan in loan approval is to answer one question above all others: will this business generate enough cash to cover its debt? The Small Business Administration, commercial banks, and alternative lenders all evaluate plans through this lens. Get that answer right, and your approval odds rise sharply.

Loan officers evaluate every application through the five Cs of credit: character, capacity, capital, collateral, and conditions. Your business plan is the primary evidence file for all five. A weak plan leaves underwriters guessing. A strong plan answers their questions before they ask.

Here is what lenders focus on most:

Pro Tip: A mediocre business with strong documentation often outperforms a strong business with weak documentation. Lenders cannot fund what they cannot verify.

The importance of business plan quality is not just about impressing a banker. It is about reducing the perceived risk of lending to you. Every section of your plan should answer a specific underwriting question, not tell a story about your passion for the industry.

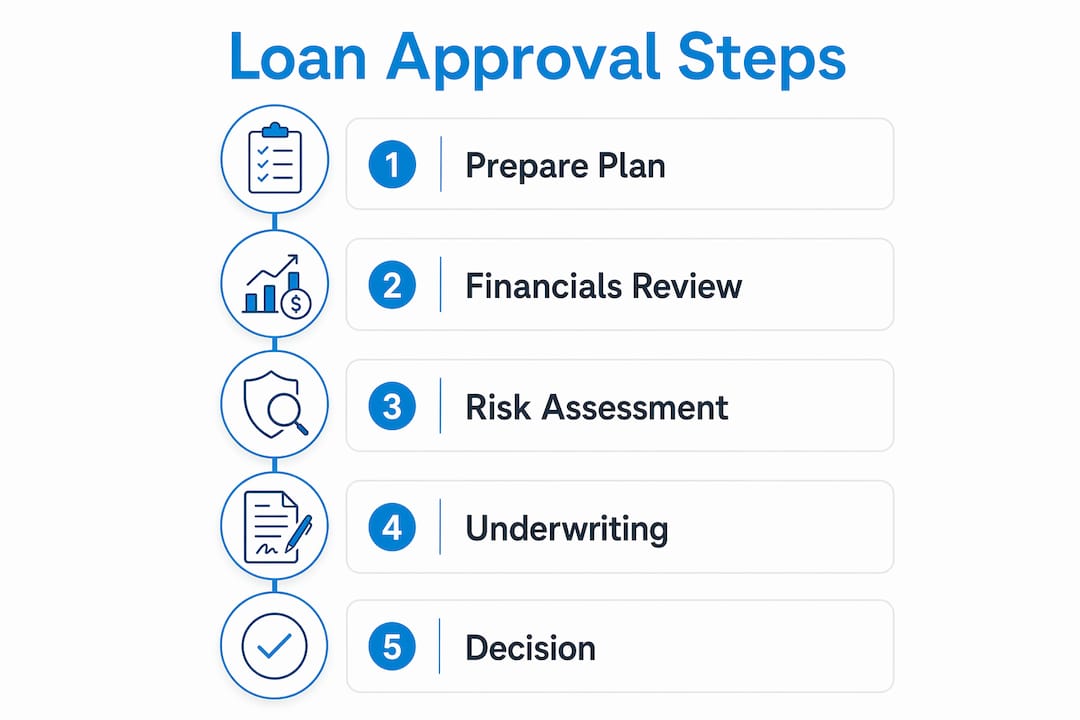

A lender-ready business plan follows the exact order that underwriters review it. Most entrepreneurs write plans in the order that feels natural to them. Underwriters read plans in the order that answers their risk questions fastest. Align your structure with theirs, and you remove friction from the approval process.

Follow this sequence:

Pro Tip: Structure your plan to mirror the underwriting review order. Answering lender questions proactively, before they have to ask, is the single fastest way to speed up approval.

The goal of every section is to reduce uncertainty. Lenders are not looking for inspiration. They are looking for evidence that you understand your business well enough to run it profitably and repay what you borrow.

Most business plan rejections trace back to a small set of predictable errors. Knowing them in advance lets you avoid them entirely.

A well-prepared business plan reduces lender perceived risk and instills confidence in your repayment ability. The inverse is equally true. A sloppy plan amplifies every concern a lender already has about small business risk.

The difference between a plan that gets approved and one that gets declined often comes down to specificity and credibility. These practices separate strong applications from weak ones.

Build month-by-month cash flow projections for year 1. Annual projections hide seasonality. A retail business that earns 40% of its revenue in November and December looks very different month-by-month than it does as an annual average. Lenders want to see that you understand your cash cycle and that you can cover loan payments in your slow months.

Use real vendor quotes in your budget. If you plan to spend $75,000 on equipment, attach a quote from the supplier. If you plan to lease a space, include the letter of intent with the monthly rent figure. Real numbers from real vendors tell lenders you have done your homework. Estimates pulled from thin air tell them the opposite.

Reference credible market research. Citing IBISWorld, the Bureau of Labor Statistics, or a National Restaurant Association report carries far more weight than writing “the market is growing rapidly.” Name the source and the specific figure.

Treat your business plan as a living document. Regularly updating your plan transforms it from a static submission into a tool that reflects your current reality. Lenders who see a plan updated within the last 90 days know you are actively managing your business, not just applying for money.

| Element | Weak version | Strong version |

|---|---|---|

| Revenue projection | “$600,000 in year 1” | “1,200 units x $500 avg. price = $600,000” |

| Use of funds | “Equipment and marketing” | “$42,000 Haas CNC lathe, $18,000 Google Ads” |

| Market analysis | “The market is growing” | “IBISWorld: 4.2% annual growth, $18B industry” |

| Management team | “Experienced leadership” | “Jane Smith, 12 years in food distribution” |

| DSCR | Not mentioned | “Projected DSCR: 1.35x in year 1” |

Check the small business funding checklist to confirm your plan covers every element lenders expect before you submit.

A business plan that directly addresses lender risk concerns, with specific financial projections, a clear use of funds, and a DSCR above 1.0x, is the single most reliable way to improve your loan approval odds.

| Point | Details |

|---|---|

| DSCR is the core metric | Show cash flow exceeds debt payments, with a minimum 1.0x ratio, ideally 1.25x or higher. |

| Structure follows underwriting order | Lead with use of funds and financial capacity, not your company story. |

| Specificity beats enthusiasm | Real vendor quotes, named data sources, and unit-level projections outperform vague estimates. |

| Avoid round numbers | Build revenue projections from units sold and price, not arbitrary percentage growth. |

| Update your plan regularly | A current plan signals active management and reduces lender uncertainty. |

The most common mistake I see from small business owners is treating the loan application as a sales pitch. They spend weeks perfecting their executive summary narrative and almost no time on the financial model. Lenders are not buying your story. They are underwriting your numbers.

I have watched businesses with genuinely strong operations get declined because their plans were vague, templated, or structurally out of order. The underwriter could not find the DSCR calculation. The use-of-funds section listed three broad categories. The revenue projections were round numbers with no supporting logic. The business was real and profitable. The documentation failed it.

The inverse happens too. A business with modest revenue but a meticulously prepared plan, with real vendor quotes, a month-by-month cash flow model, and a clear DSCR analysis, gets approved faster and often at better terms. Lenders see business plans as risk-assessment documents, not sales brochures. The quality of your documentation is a direct signal of how you run your business.

Treat your business plan as an operating system, not a formality. Refine it every quarter. Build it around the questions an underwriter will ask, not the story you want to tell. That shift in mindset is what separates funded businesses from rejected ones.

— Rob

You have built a plan that addresses lender risk, shows a credible DSCR, and includes a detailed use-of-funds budget. Now you need a lender who will actually read it.

Fordhamcapital has funded over $120M for small and medium-sized businesses, helping clients generate more than $500M in revenue. With an A+ BBB rating, a one-page application, and approvals within 24 hours, Fordhamcapital connects you to a wide network of banks and lenders without impacting your credit. Your well-prepared plan deserves a fast, fair review. Start your application today and put your documentation to work.

A business plan is the primary risk assessment document lenders use to evaluate whether a business can repay a loan. It demonstrates cash flow capacity, use of funds, and management credibility.

Lenders require month-by-month projections for year 1 and annual projections for years 2 through 5, with a DSCR above 1.0x shown explicitly.

Every expense should be broken down by category with real vendor estimates where possible. Vague categories like “equipment” are not sufficient for underwriting review.

A strong plan reduces perceived risk and can improve your terms, but it does not replace credit history entirely. It works best when paired with solid financials and a clear repayment path.

Update your plan at least every 90 days. A current plan reflects active management and gives lenders confidence that your projections are grounded in your current business reality.

At Fordham Capital, we've made the application process straightforward and reassuring. Dive in and explore your financial options with confidence, knowing there's no impact on your credit score and no obligations. We review your details and offer customized solutions based on what you're looking for.