Protecting your credit score during business borrowing is the single most important financial discipline a small business owner can practice. Your credit score, both personal and business, determines the interest rates you qualify for, the loan amounts lenders approve, and whether you get funded at all. Borrowing without a plan to protect credit score business borrowing outcomes can quietly erode years of credit history in a matter of months. The good news is that with the right structure in place, you can grow your business and keep your credit profile intact at the same time.

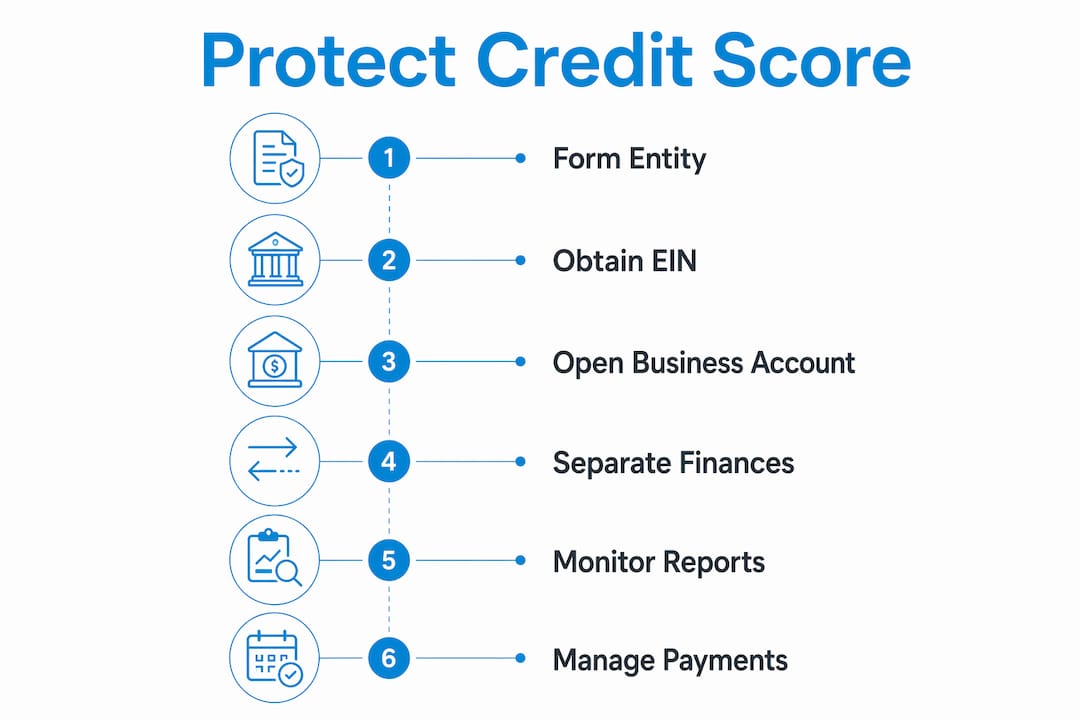

The foundation of credit score protection starts before you ever apply for a loan. The U.S. Small Business Administration confirms that without an EIN and legal entity, lenders default to your personal credit for underwriting. That means every business loan, every hard inquiry, and every missed payment lands directly on your personal credit report.

Forming an LLC or corporation creates a legal wall between you and your business. That wall does not protect you automatically, but it gives lenders a separate entity to evaluate. Once that entity has its own credit history, lenders have less reason to pull your personal report.

The practical steps to separate your credit identities are straightforward:

Mixing personal and business finances delays business credit building and increases the risk to your personal score. Lenders who see commingled finances treat the business as an extension of you personally, which defeats the purpose of separating the entities.

Pro Tip: Open your business bank account the same week you receive your EIN. The longer your business account has been active, the stronger your business credit profile looks to lenders.

Business credit does not build automatically after incorporation. Active management and proper vendor relationships that report to bureaus are required to establish a strong score. This surprises many first-time business owners who assume their company credit builds the same way personal credit does.

Three bureaus dominate business credit reporting: Dun & Bradstreet, Experian Business, and Equifax Business. Each uses its own scoring model. D&B uses the PAYDEX score, which runs from 0 to 100. Experian Business uses the Intelliscore Plus. Equifax Business uses the Business Credit Risk Score. Lenders often check all three when evaluating a loan application, so your score on each bureau matters.

Here is the fastest path to building a strong business credit profile:

| Bureau | Score Name | Score Range | Key Factor |

|---|---|---|---|

| Dun & Bradstreet | PAYDEX | 0–100 | Payment timing |

| Experian Business | Intelliscore Plus | 0–100 | Payment history, utilization |

| Equifax Business | Business Credit Risk Score | 101–992 | Delinquency risk |

Disputing errors on business credit reports is something you can do yourself. Business credit repair does not require expensive third-party services. Pull your reports, identify inaccuracies, and submit disputes directly to each bureau with supporting documents.

Pro Tip: Set a calendar reminder every 90 days to pull your business credit reports from all three bureaus. Errors left uncorrected for months can cost you loan approvals.

Personal credit and business credit are separate systems, but they interact more than most owners realize. Some loans and credit cards report activity to both personal and business bureaus. Knowing which products report where is one of the most underused credit protection strategies available.

Personal guarantees are common in small business lending. When you sign a personal guarantee, you agree that if the business defaults, you are personally liable. That liability shows up on your personal credit report. Choosing funding products that do not require personal guarantees, or that report only to business bureaus, keeps your personal score insulated from business risk. Fordhamcapital’s funding approach is built around this reality, connecting business owners to lenders who understand the difference.

“The most effective way to protect your personal credit during business borrowing is to build a business credit profile strong enough that lenders do not need to rely on your personal score at all. That takes time and deliberate action, but it is achievable within 12–24 months for most business owners.”

Understanding how business funding impacts your personal credit score before you apply is the difference between a funding decision that helps you grow and one that quietly damages your financial standing.

The most common credit mistakes are not dramatic. They are quiet, gradual, and entirely avoidable. Recognizing them early is the fastest way to protect your credit profile.

Applying for too many credit lines at once is the most frequent error. Each application triggers a hard inquiry. Multiple inquiries in a short period signal financial stress to lenders, even when the business is healthy. Space out applications by at least 90 days when possible.

Failing to confirm vendor reporting is a costly oversight. Not every vendor that offers net-30 terms reports payment history to business bureaus. If your payments are not being reported, you are building goodwill with a supplier but not building credit. Always ask vendors directly whether they report to Dun & Bradstreet, Experian Business, or Equifax Business before opening an account.

Ignoring past-due accounts causes compounding damage. Resolving debts and negotiating payment plans with creditors prevents further damage and signals responsibility to future lenders, even when the score improvement takes time to appear.

Additional mistakes that consistently harm credit scores include:

Owners who want to rebuild business credit while borrowing need to treat credit management as an ongoing operational task, not a one-time fix. The businesses that maintain strong credit profiles are the ones that check their reports, pay early, and separate their finances from day one.

Protecting your credit score during business borrowing requires separating your finances, building business credit actively, and monitoring both personal and business reports on a regular schedule.

| Point | Details |

|---|---|

| Separate your entities | Form an LLC or corporation and get an EIN before applying for any business funding. |

| Build business credit actively | Open net-30 vendor accounts that report to bureaus and pay 10–15 days early to maximize PAYDEX scores. |

| Know what lenders pull | Some loans trigger personal credit inquiries; choose products that report only to business bureaus when possible. |

| Keep utilization below 30% | Pay balances frequently and request credit limit increases to protect both personal and business scores. |

| Monitor and dispute regularly | Pull reports from all three business bureaus every quarter and dispute errors with documentation immediately. |

Most business owners treat credit protection as a defensive move. I think that framing is wrong. Building a strong business credit profile is an offensive growth strategy. When your business credit score is solid, you qualify for larger loan amounts at lower rates, and lenders compete for your business rather than the other way around.

The part that surprises owners most is the timeline. Credit does not respond quickly to good behavior. You can do everything right, pay early, keep utilization low, dispute errors, and still wait 12–18 months before your score reflects those habits. That gap between action and reward is where most people give up. The owners who push through it are the ones who eventually borrow on their own terms.

One thing I tell every business owner: start building credit before you need it. The worst time to establish a D-U-N-S Number or open vendor accounts is when you are already in a cash crunch and need funding in 30 days. Lenders look at the age of your accounts, and a two-month-old business credit file is not going to impress anyone. Build the foundation now, even if you do not plan to borrow for another year.

The other piece of advice that rarely gets said clearly: you do not need to pay anyone to repair your business credit. Business owners can repair credit themselves by pulling reports, disputing errors, paying down balances, and building positive payment history. Save that money and put it toward the business instead.

— Rob

Small business owners who need capital quickly often face a painful tradeoff: apply for funding and risk a hard inquiry on their personal credit, or hold off and miss a growth opportunity.

Fordhamcapital was built to remove that tradeoff. With a one-page application, approvals within 24 hours, and access to a wide network of banks and lenders, Fordhamcapital connects business owners to funding options that fit their credit profile rather than forcing them into products that damage it. The company holds an A+ BBB rating and has funded over $120M for businesses across the country. If you are ready to apply for business funding without the credit guesswork, Fordhamcapital is the place to start. You can also explore the full range of fast and flexible funding options available to small business owners today.

Separate your personal and business finances immediately by forming a legal entity, obtaining an EIN, and opening dedicated business accounts. This prevents business borrowing activity from appearing on your personal credit report.

It depends on the loan type and lender. Many business loans require a personal guarantee and trigger a hard inquiry on your personal credit. Choosing products that report only to business bureaus reduces this risk.

Building a solid business credit profile typically takes 12–24 months of consistent on-time or early payments, active vendor accounts, and regular monitoring. Starting before you need funding gives you the strongest position.

Yes. Business owners can repair credit themselves by pulling reports from Dun & Bradstreet, Experian Business, and Equifax Business, disputing errors with documentation, and paying down outstanding balances.

Keep credit utilization below 30% on both personal and business credit accounts. Paying balances more frequently than once a month is the most direct way to hold utilization at a safe level.

At Fordham Capital, we've made the application process straightforward and reassuring. Dive in and explore your financial options with confidence, knowing there's no impact on your credit score and no obligations. We review your details and offer customized solutions based on what you're looking for.