Non-credit-reporting business funding options are financing products that approve businesses based on revenue, invoices, or sales history rather than a hard credit inquiry. Small business owners with thin credit files, past financial setbacks, or simply a desire to protect their credit scores use these products to access capital fast. The industry term for this category is “alternative business funding,” and it covers everything from merchant cash advances to nonprofit microloans. Fordhamcapital has funded over $120M using this approach, helping clients generate more than $500M in revenue without relying on traditional credit checks.

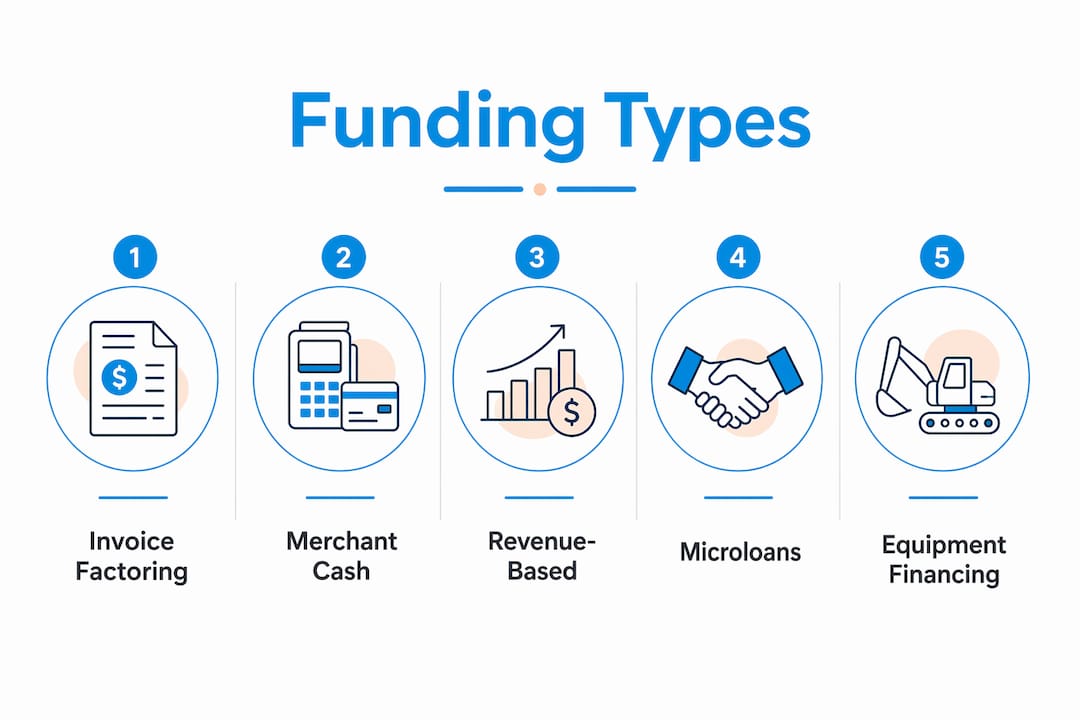

Alternative business funding breaks into five practical categories. Each one evaluates your business differently, so matching the right product to your situation matters more than picking the one with the lowest advertised rate.

Merchant cash advances (MCAs) give you a lump sum in exchange for a percentage of future sales. Repayment happens automatically as a daily or weekly deduction from your card receipts. Payment processor loans work the same way, basing approval on sales data instead of credit reports. Both products fund quickly, often within 24–48 hours, but carry the highest costs in this category.

Invoice factoring lets you sell unpaid invoices to a third party called a factor. The factor advances 70%–90% of the invoice value upfront and collects payment directly from your customers. The factor evaluates your customers’ creditworthiness, not yours. This makes invoice factoring especially useful for B2B businesses with slow-paying clients, since it reduces cash flow volatility and improves working capital without a hard credit pull.

Revenue-based financing ties repayment to a fixed percentage of monthly revenue. When sales are strong, you pay more. When sales dip, you pay less. Lenders look at your sales history, typically three to six months of bank statements or payment processor data, to set terms.

Microloans from nonprofit and community lenders offer smaller amounts, usually under $50,000, to startups and credit-challenged businesses. Nonprofit microlenders like Kiva evaluate business viability rather than credit scores, though most require no active bankruptcy, foreclosure, or liens.

Equipment financing is a fifth option worth knowing. The equipment itself serves as collateral, which reduces lender risk and often eliminates the need for a hard credit check entirely.

| Funding type | Primary approval factor | Typical advance or amount | Repayment structure |

|---|---|---|---|

| Merchant cash advance | Daily sales volume | Varies by revenue | % of daily sales |

| Invoice factoring | Customer creditworthiness | 70%–90% of invoice | Collected from customers |

| Revenue-based financing | Sales history | Varies | % of monthly revenue |

| Nonprofit microloan | Business viability | Under $50,000 | Fixed monthly payments |

| Equipment financing | Equipment value | Up to equipment cost | Fixed monthly payments |

Pro Tip: Compare total repayment amounts across all options, not just the stated rate. A microloan at a higher nominal rate can cost far less in total dollars than a merchant cash advance with a low-sounding factor rate.

Qualification for these products focuses on business performance, not personal credit history. Lenders want proof that your business generates enough revenue to repay the advance or loan. The specific documents they request depend on the product type.

Most lenders ask for:

Soft credit pulls appear in some revenue-based financing approvals. A soft inquiry does not affect your credit score. It differs from a hard inquiry, which lenders use for traditional loans and which can lower your score by several points. Knowing this distinction matters if you are actively protecting your credit profile. You can read more about how funding affects your credit score before you apply.

Eligibility constraints vary by product. MCAs typically require at least three months in business and a minimum monthly revenue threshold. Nonprofit microloans may require a business plan and proof of community impact. Equipment financing requires the equipment to hold resale value. Industry restrictions also apply. Some lenders exclude high-risk sectors like cannabis, gambling, or firearms.

Organized financial records speed up approval and improve your chances with nontraditional lenders. Applicants who submit clean, current bank statements and payment processor reports consistently receive faster decisions.

Pro Tip: Pull your last six months of bank statements and payment processor reports before you start any application. Having them ready cuts the approval timeline and signals to lenders that your business is well-managed.

Speed and accessibility come at a price. Unsecured business loans carry interest rates ranging from 7%–75% APR depending on the lender and the risk profile of your business. That range is wide because lenders price for the absence of collateral and the reduced role of credit history.

Merchant cash advances sit at the expensive end of the spectrum. MCAs often carry triple-digit effective APRs and are designed as short-term bridge financing, not long-term capital. The problem is that many business owners treat them as recurring funding, rolling one advance into the next. That cycle compounds costs quickly.

A specific risk with MCAs is the lack of clear APR disclosure. Factor rates (expressed as 1.2x or 1.4x the advance amount) do not translate directly into APR, which makes cost comparisons difficult. Always calculate total repayment before signing. If you borrow $50,000 at a 1.4 factor rate, you repay $70,000 regardless of how fast you pay it off.

Short repayment terms and high fees can strain cash flow, particularly for seasonal businesses. When daily sales deductions hit during a slow month, the pressure compounds. Revenue-based financing handles this better because payments flex with revenue, but the total cost can still exceed traditional loan options.

| Funding type | Typical cost range | Repayment term | Key risk |

|---|---|---|---|

| Merchant cash advance | Triple-digit effective APR | 3–18 months | Cash flow strain in slow periods |

| Invoice factoring | 1%–5% of invoice per month | Until invoice is paid | Customer payment delays |

| Revenue-based financing | 6%–50% APR equivalent | 12–36 months | Total cost exceeds expectations |

| Nonprofit microloan | 8%–13% APR | 12–60 months | Smaller amounts, slower process |

| Equipment financing | 7%–30% APR | 24–72 months | Equipment depreciation risk |

No-credit-check loans provide the fastest capital access but consistently carry the highest costs. Use them as short-term solutions, not permanent financing strategies.

Choosing the right product starts with an honest assessment of your business situation. Work through these steps before you apply anywhere.

Define your funding amount and timeline. Do you need $10,000 in 48 hours or $100,000 within two weeks? Urgency narrows your options fast. MCAs and payment processor loans fund the quickest. Microloans take the longest.

Audit your revenue and invoice portfolio. If you carry significant accounts receivable from creditworthy business customers, invoice factoring may cost less than an MCA and solve the same cash flow problem. If your revenue is steady and predictable, revenue-based financing gives you more repayment flexibility.

Calculate total repayment, not just the rate. Comparing total repayment amounts gives a more accurate cost picture than comparing nominal interest rates alone. A product with a lower rate but a longer term can cost more in total dollars.

Verify lender credibility. Check for a Better Business Bureau rating, read third-party reviews, and confirm the lender discloses all fees upfront. Fordhamcapital holds an A+ BBB rating and provides full fee transparency before any commitment.

Read the repayment terms for hidden fees. Watch for origination fees, prepayment penalties, and renewal fees. These add to the total cost and rarely appear in the headline offer.

Match the funding term to the business need. Use short-term, higher-cost products only for short-term needs like covering a payroll gap or purchasing inventory before a peak season. For longer-term growth capital, explore funding without collateral or microloan programs with lower total costs.

Pro Tip: Never accept the first offer you receive. Get at least two competing term sheets and compare total repayment, not factor rates or APR alone. The difference can be thousands of dollars.

Non-credit-reporting business funding options provide real capital access for businesses that cannot or choose not to use traditional credit-based lending, but the cost and repayment structure vary dramatically by product type.

| Point | Details |

|---|---|

| Approval based on revenue, not credit | Lenders evaluate sales history, invoices, or equipment value instead of your credit score. |

| Invoice factoring advances 70%–90% | Factors pay most of the invoice upfront and collect from your customers directly. |

| MCAs carry the highest costs | Effective APRs can reach triple digits; use them only for short-term bridge needs. |

| Soft pulls protect your credit score | Some revenue-based lenders use soft inquiries, which do not affect your credit profile. |

| Total repayment beats rate comparison | Always calculate the full dollar amount you will repay before choosing a product. |

The biggest misconception I see is that “no credit check” means “no consequences.” It does not. These products skip the credit inquiry, but they do not skip the cost. Business owners who treat a merchant cash advance as free money because it did not ding their credit score often find themselves in a repayment cycle that drains cash flow for months.

The products I consistently recommend first are invoice factoring and nonprofit microloans. Invoice factoring works especially well for B2B businesses sitting on unpaid invoices. You already earned that revenue. Factoring just accelerates when you receive it. The cost is real, but it is predictable and tied to a specific transaction.

Microloans get overlooked because the amounts seem small. But for a startup that needs $15,000 to buy equipment or cover initial inventory, a microloan at 10% APR beats an MCA at 150% effective APR by a wide margin. The application takes longer, but the total cost difference is not close.

My honest advice: treat urgency as a cost multiplier. The faster you need the money, the more you will pay for it. If you have even two weeks of runway, use that time to explore more than one product. The business owners who fare best with alternative funding are the ones who apply before they are desperate, compare at least two offers, and calculate total repayment before they sign anything. Speed is a feature you pay for. Make sure you actually need it.

— Rob

Fordhamcapital was built for business owners who need capital without the friction of traditional bank lending. The application takes one page, approvals happen within 24 hours, and the process does not rely on hard credit checks that damage your score.

Fordhamcapital connects you to a wide network of banks and lenders, which means you get competing offers rather than a single take-it-or-leave-it decision. With an A+ BBB rating and over $120M funded, the track record speaks for itself. If you are ready to move forward, apply now and get a funding decision without the credit impact. You can also explore the full range of business funding solutions available through Fordhamcapital to find the right fit for your stage and revenue profile.

Non-credit-reporting business funding refers to financing products that approve businesses based on revenue, invoices, or sales data rather than submitting a hard credit inquiry to the major credit bureaus. These products do not appear on your personal credit report as a new inquiry.

Most do not, especially when lenders use soft credit pulls or no credit check at all. Soft inquiries do not affect your credit score, unlike hard inquiries used in traditional loan applications.

Merchant cash advances and payment processor loans are the fastest, often funding within 24–48 hours. They base approval entirely on sales volume, which allows lenders to make quick decisions without a credit review.

Merchant cash advances are designed as short-term bridge financing, not long-term capital. Their effective APRs can reach triple digits, and rolling one advance into the next compounds costs quickly and strains cash flow.

Most lenders require three to six months of business bank statements, payment processor reports, and proof of business registration. Invoice factoring applications also require accounts receivable aging reports to evaluate your customers’ payment history.

At Fordham Capital, we've made the application process straightforward and reassuring. Dive in and explore your financial options with confidence, knowing there's no impact on your credit score and no obligations. We review your details and offer customized solutions based on what you're looking for.

.jpg)