Choosing the right lender for your small business is the single most consequential financing decision you will make. The wrong match costs you in fees, delays, and terms that strangle cash flow. The right match gives you capital at a rate your business can actually absorb. This guide covers how to select a business lender by walking through your financing needs, the lender types available, how to compare small business loan options, and how to build an application that gets approved.

The first step is knowing exactly what you need before you talk to any lender. Borrowers who skip this step end up applying for products that do not fit their situation, wasting time and triggering unnecessary credit inquiries.

Start with the loan amount. Be specific. A vague request signals to lenders that you have not done your homework. Next, identify the purpose: equipment purchase, working capital, inventory, or expansion. Lenders price risk differently depending on how the money gets used.

Your credit profile is the next filter. Most traditional lenders want a personal credit score above 680. Business credit scores, tracked by agencies like Dun & Bradstreet and Experian Business, matter just as much for established companies. Many lenders require $100,000 or more in annual revenue to qualify, though online lenders apply more flexible thresholds. That gap between traditional and online lender requirements is exactly where many small businesses find their best options.

Business age also shapes your choices. Lenders generally treat businesses under two years old as higher risk. Startups often need to look at SBA Microloans or Community Development Financial Institutions rather than conventional bank products.

| Criteria | What lenders look for |

|---|---|

| Credit score | Personal 680+; business score varies by lender |

| Annual revenue | $100,000+ typical; online lenders more flexible |

| Time in business | 2+ years preferred; startups have limited options |

| Loan purpose | Equipment, working capital, expansion, real estate |

| Collateral | Assets reduce lender risk and improve terms |

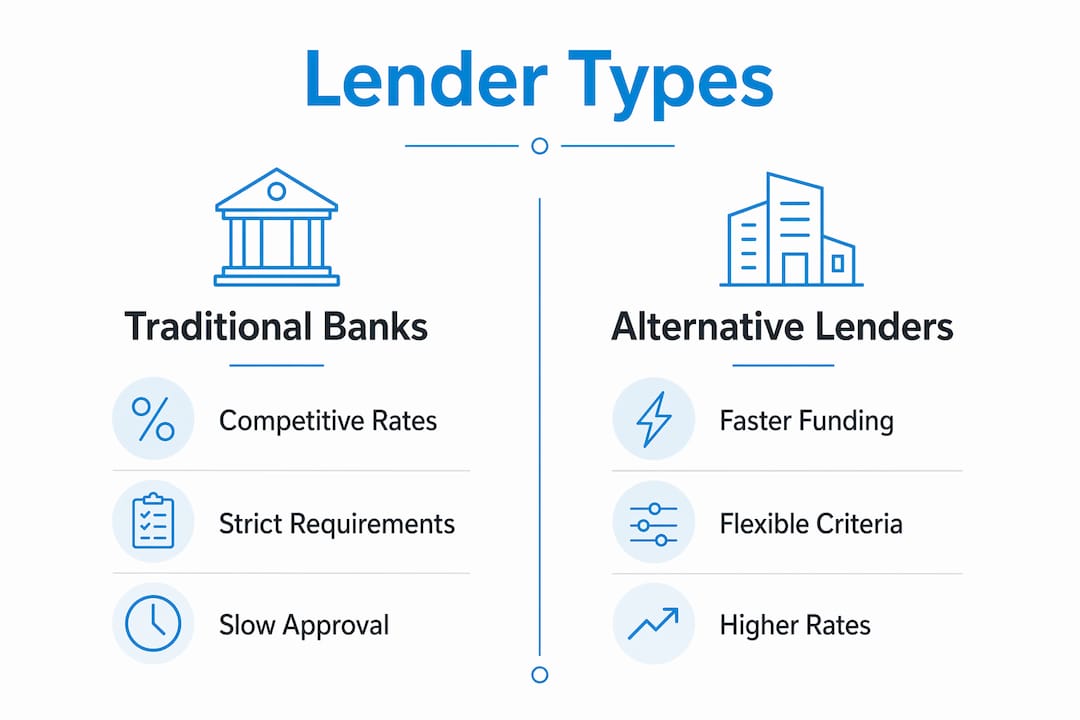

The lender category you target determines your rate, speed, and approval odds. Each type serves a different borrower profile.

Traditional banks and credit unions offer the most competitive interest rates, but they also carry the strictest requirements. They favor businesses with strong credit, two or more years of history, and solid collateral. If you qualify, the savings on interest are real. If you do not, the application process wastes weeks.

SBA-approved lenders offer government-backed products that reduce lender risk, which translates into better terms for borrowers. The SBA 7(a) loan goes up to $5,000,000 and bases eligibility on income, credit history, and business location. SBA lenders operate at significant scale. Top SBA lenders originate billions annually, which reflects their experience processing complex applications. That volume matters because experienced lenders make fewer errors that delay funding.

SBA Microloans fill the gap for startups and businesses with limited credit history. These loans go up to $50,000, with an average loan around $13,000 and interest rates between 8% and 13%. They are distributed through nonprofit community intermediaries who also provide business guidance alongside funding. That combination of capital and coaching makes Microloans especially valuable for first-time borrowers.

Online and alternative lenders approve faster and ask fewer questions about business history. The tradeoff is higher rates. For businesses that need capital within days rather than weeks, the speed premium is often worth paying. You can learn more about this category in this guide to non-bank financing.

Community Development Financial Institutions (CDFIs) serve underbanked markets and businesses in low-income areas. They accept lower credit scores and thinner financial histories than banks, making them a strong option for newer businesses or owners rebuilding credit.

| Lender type | Best for | Typical speed |

|---|---|---|

| Traditional bank | Established businesses, strong credit | Weeks to months |

| SBA-approved lender | Businesses needing larger amounts, better terms | 30–90 days |

| SBA Microloan | Startups, thin credit history | 2–4 weeks |

| Online lender | Fast capital, flexible criteria | 1–5 business days |

| CDFI or microlender | Underserved markets, rebuilding credit | 1–4 weeks |

Pro Tip: Use the SBA Lender Match tool at sba.gov to get connected with SBA-approved lenders in your area based on your specific business profile. It takes under five minutes and produces real lender referrals.

Comparing loans on interest rate alone is a mistake. The annual percentage rate (APR) captures the full cost of borrowing, including origination fees, closing costs, and other charges. Two loans with identical stated rates can carry very different APRs.

Understanding fixed versus variable interest rates, along with fees and repayment schedules, is the foundation of smart loan comparison. Fixed rates give you predictable monthly payments. Variable rates start lower but can rise with market conditions, which creates cash flow risk for businesses with tight margins.

Funding speed is a factor that most guides underweight. SBA loan approvals take 30–90 days. If you need capital to cover payroll next week, an SBA loan is not your answer regardless of how good the rate is. Matching funding timeline to your actual need is as important as matching the rate.

Short-term loans dominate small business approvals, but medium-term and SBA loans provide larger amounts and longer repayment windows. Longer terms lower your monthly payment but increase total interest paid. Run both scenarios before committing.

Key factors to scrutinize when comparing loan options:

Pro Tip: Ask every lender for the full fee schedule in writing before you apply. Verbal quotes are not binding. Written disclosures are.

A strong application reduces approval time and improves your terms. Lenders reward organized borrowers with faster decisions. Disorganized applications signal operational risk.

Gather these documents before you contact any lender:

Credit readiness matters before you submit. Pull your personal and business credit reports and dispute any errors. Even a 20-point improvement in your credit score can shift you into a better rate tier. Pay down revolving balances where possible before applying.

Avoid the most common application pitfalls. Do not apply to multiple lenders simultaneously without understanding that each hard inquiry can lower your score. Do not overstate revenue or understate debt. Lenders verify both, and discrepancies kill applications. Use the SBA Lender Match tool to identify lenders whose criteria match your profile before you formally apply. You can also review this funding checklist to make sure you have covered every requirement.

Selecting the right lender requires matching your credit profile, loan purpose, and timeline to the lender type that serves those needs best.

| Point | Details |

|---|---|

| Know your criteria first | Define loan amount, purpose, and credit profile before approaching any lender. |

| Match lender type to your profile | SBA loans suit established businesses; Microloans and CDFIs serve startups and thin-credit borrowers. |

| Compare APR, not just rate | Origination fees and penalties change the true cost of any loan significantly. |

| Funding speed is a real factor | SBA approvals take 30–90 days; online lenders can fund in days when timing is critical. |

| Prepare documents in advance | Organized applications get faster decisions and better terms from every lender type. |

Most articles on finding reliable business financing treat lender selection like a product comparison exercise. Pick the lowest rate, check the boxes, apply. That framing misses the most important variable: the relationship.

I have seen business owners secure capital from lenders who were not the cheapest option, and they came out ahead. Why? Because when their business hit a rough quarter, that lender picked up the phone and worked with them on a modified payment schedule. A lender who treats you like a file number will not do that.

Speed and cost are real factors, but they are not the whole picture. The lender who funds you in 48 hours at a higher rate may be the right call if you are closing a contract that triples your revenue. The lender who takes 60 days at a lower rate may be the right call if you are funding a three-year equipment purchase. Context determines the answer, not a rate table.

My honest advice: talk to at least three lenders before you commit. Ask each one what happens if you miss a payment. Ask how they handle early payoff. Ask whether your account will be managed by a person or a portal. Those answers tell you more about the relationship than any rate sheet. For a deeper look at how lender networks operate, this guide to funding networks is worth your time.

Borrower education is not a nice-to-have. It is the difference between a loan that works for your business and one that works against it.

— Rob

Small business owners who need capital without the delays of traditional lending have a direct path forward with Fordhamcapital. The one-page application does not trigger a credit inquiry, and approvals arrive within 24 hours. Fordhamcapital connects borrowers to a wide network of banks and lenders, which means your profile gets matched to the product that fits rather than forced into a single bank’s criteria.

Fordhamcapital holds an A+ BBB rating, has funded over $120,000,000, and has helped clients generate more than $500,000,000 in revenue. If you are ready to move, apply for funding today and get a decision without the wait. You can also visit Fordhamcapital.com to review tailored options before you commit.

Start by defining your loan amount, purpose, and credit profile. Then match those factors to the lender type that serves your situation, whether that is a traditional bank, SBA-approved lender, online lender, or CDFI.

Most traditional lenders require a personal credit score above 680. Online lenders and CDFIs accept lower scores, though higher rates apply. Business credit scores from agencies like Dun & Bradstreet also factor into decisions for established companies.

SBA loan approvals typically take 30–90 days. Online lenders can fund in one to five business days. Fordhamcapital offers approvals within 24 hours through its lender network.

An SBA Microloan provides up to $50,000 through nonprofit community intermediaries, with interest rates between 8% and 13%. Startups and businesses with limited collateral or credit history are the primary candidates.

Most lenders require two to three years of tax returns, recent profit and loss statements, bank statements, a business plan, and legal business documents. Having these ready before you apply speeds up the process and signals to lenders that you are prepared.

At Fordham Capital, we've made the application process straightforward and reassuring. Dive in and explore your financial options with confidence, knowing there's no impact on your credit score and no obligations. We review your details and offer customized solutions based on what you're looking for.

.jpg)