Business funding without strong credit is defined by alternative underwriting models that prioritize cash flow, revenue consistency, and bank deposit stability over FICO scores. Traditional banks reject most applicants with scores below 680, but non-bank lenders and revenue-first programs fill that gap. Understanding how funding works without strong credit means knowing which factors actually drive approval decisions and which products are built for businesses in your position.

Alternative funding options for businesses with low credit scores fall into several distinct categories, each with different qualification criteria and repayment structures. The right choice depends on your monthly revenue, how long you have been in business, and what assets you can bring to the table.

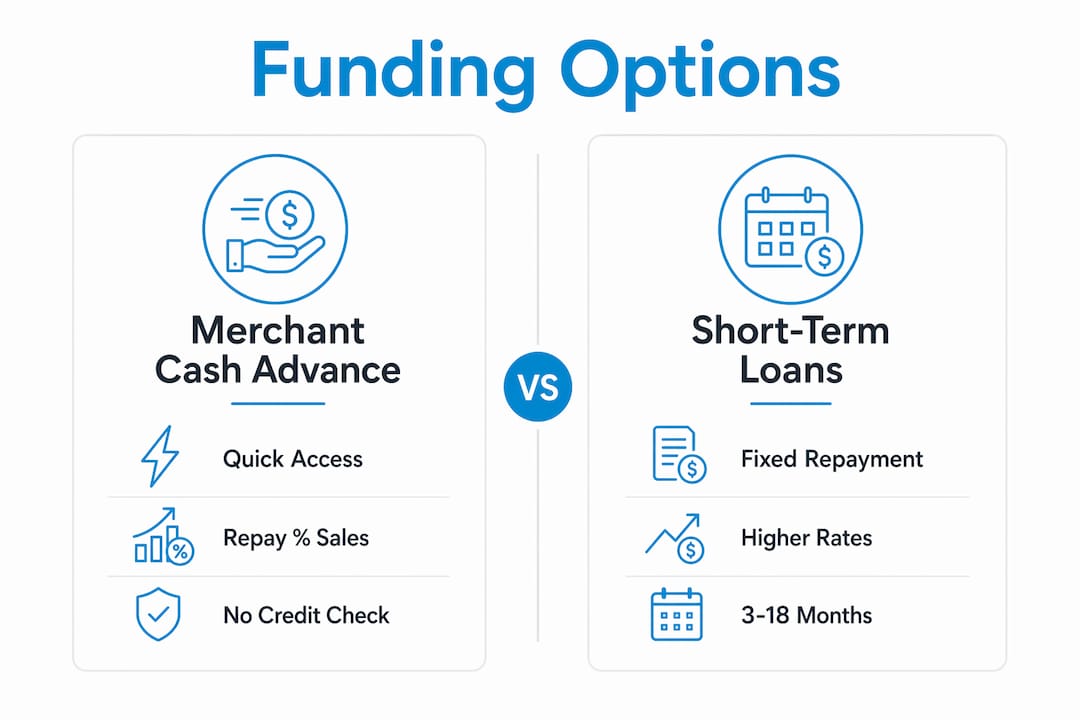

Merchant cash advances (MCAs) are the most accessible option for businesses with poor credit. MCAs provide a lump sum upfront, repaid as a fixed percentage of daily or weekly sales. Approval depends almost entirely on revenue volume, not credit history.

Revenue-based financing works similarly but typically offers longer repayment windows. Lenders review three to six months of bank statements and fund based on average monthly deposits. Businesses with credit scores as low as 500–520 can qualify by showing monthly deposits of $10,000 to $25,000.

Here are the primary financing options available to business owners with low credit:

Lenders assess several non-credit factors during prequalification: average monthly bank deposits, number of months in business, frequency of overdrafts, and overall bank balance trends. Most of these assessments use a soft credit pull, which does not affect your score.

Pro Tip: Use soft-pull prequalification tools before submitting any formal application. Comparing multiple offers costs you nothing and protects your credit score from hard inquiry damage.

Revenue consistency outweighs credit scores in alternative lender underwriting models. A business with strong, stable deposits but a 540 credit score will often out-qualify a business with a 620 score and erratic revenue. That is a fundamental shift from how traditional banks think about risk.

Lenders using revenue-first underwriting evaluate applicants through a specific set of criteria:

“Underwriters prioritize cash flow consistency and the absence of overdrafts more than raw revenue volume or credit score. Stable, predictable deposits are the single most persuasive factor in a revenue-first approval decision.”

Legitimate lenders emphasize comprehensive financial assessment over simple credit scores to determine funding eligibility and rates. Any lender claiming guaranteed approval without reviewing any financial information is not a legitimate lender. That claim is a red flag, not a selling point.

Understanding what lenders actually look for gives you a real advantage. You can review your own bank statements before applying and address obvious weaknesses, like a month with an overdraft or a dip in deposits, before they become reasons for denial. For a deeper breakdown of what drives approval decisions, the guide on loan approval factors covers the full picture.

Financing with bad credit costs more. That is not a judgment. It is the math of risk pricing. Lenders charge higher rates to offset the statistical likelihood of default among borrowers with weaker credit profiles. Knowing what to expect helps you plan and avoid surprises.

| Funding type | Typical repayment structure | Cost indicator |

|---|---|---|

| Merchant cash advance | Fixed % of daily or weekly sales | Factor rates of 1.2–1.5 |

| Short-term working capital loan | Fixed daily or weekly payments | Higher APR than bank loans |

| Equipment financing | Monthly installments | Moderate, collateral reduces cost |

| Invoice factoring | Lender keeps a discount on invoice value | Fee per invoice, typically 1–5% |

| Revenue-based financing | % of monthly revenue until repaid | Varies by lender and revenue |

MCAs do not use traditional interest rates. They use factor rates, which means a $20,000 advance with a 1.3 factor rate costs $26,000 total regardless of how fast you repay. Paying it off early does not reduce the cost the way it would with a standard loan.

Short-term loans typically run 3–18 months. The shorter the term, the higher the effective annual percentage rate, even if the total dollar cost is lower. A $15,000 loan repaid over six months at a flat fee can carry an APR well above 50%.

Pro Tip: Calculate the total cost of capital, not just the monthly payment. Divide the total repayment amount by the amount you received, then factor in the repayment timeline. That number tells you the real cost.

The strategic use of high-rate, short-term loans is worth considering. Consistent on-time payments for 6–12 months are often reported to business credit bureaus and improve credit profiles. That means a well-managed MCA or short-term loan today can open the door to lower-cost capital in 12 months. It is a deliberate credit-building strategy, not just a stopgap.

Improving your funding profile does not require fixing your credit score overnight. It requires making your business financials look as strong as possible to the lenders who actually evaluate them. Several practical steps move the needle quickly.

Comparing multiple offers is critical for borrowers with bad credit because fees and interest rates vary widely across lenders. A difference of 10 percentage points in effective rate on a $30,000 loan is a $3,000 difference in total cost. That gap is worth the time it takes to compare. You can also explore funding options without collateral if securing assets is not currently an option.

Funding without strong credit works when you shift focus from your credit score to your cash flow, deposit consistency, and repayment track record.

| Point | Details |

|---|---|

| Revenue beats credit score | Consistent monthly deposits often qualify a business even with a score as low as 500. |

| Overdrafts kill applications | A single overdraft in your review window signals cash flow risk and can trigger denial. |

| MCAs repay from sales | Merchant cash advances take a fixed percentage of daily revenue, not a fixed monthly payment. |

| Short-term loans build credit | On-time payments for 6–12 months are reported to business credit bureaus and improve your profile. |

| Soft pulls protect your score | Always prequalify with a soft credit check before submitting a formal application. |

The most common mistake I see business owners make is treating a low credit score as a permanent disqualifier. It is not. Credit is one data point. Revenue is another. Lenders who specialize in small business funding know this, and the good ones build their entire underwriting model around it.

What actually matters is whether your business generates predictable cash. I have seen businesses with 520 credit scores get funded in 48 hours because their bank statements told a clear story: consistent deposits, no overdrafts, and a growing average balance. That story is more persuasive than a 680 score with volatile revenue.

The part most articles skip is the cost conversation. High-rate funding is not inherently bad. It is bad when you use it without a plan. If you take a short-term loan at a high rate, deploy it to generate revenue that exceeds the cost, and then use the payment history to refinance at a lower rate, you have used expensive capital intelligently. That is a strategy, not desperation.

My honest advice: stop trying to fix your credit before you apply. Start by cleaning up your bank statements. Three months of clean, consistent deposits with no overdrafts will do more for your approval odds than six months of credit repair. Then use soft-pull prequalification to understand what you actually qualify for before you commit to anything.

— Rob

Fordhamcapital was built for exactly this situation. If your credit score is not where you want it to be, but your business generates real revenue, Fordhamcapital’s funding process evaluates what actually matters. The one-page application takes minutes, approvals come within 24 hours, and the process does not trigger a hard credit inquiry.

Fordhamcapital has funded over $120M for small and medium-sized businesses, helping clients generate more than $500M in revenue. The A+ BBB rating reflects a track record of transparent terms and honest guidance. If you are ready to see what you qualify for without risking your credit score, apply for funding and get a clear answer fast.

Businesses with scores as low as 500–520 can qualify for merchant cash advances or revenue-based financing by showing monthly deposits of $10,000 to $25,000. Credit score matters less than deposit consistency.

A merchant cash advance repays as a fixed percentage of daily or weekly sales, while a short-term loan uses fixed scheduled payments. MCAs flex with your revenue; short-term loans do not.

Prequalification uses a soft credit pull, which does not affect your score. Only a formal application triggers a hard inquiry, so always prequalify first before committing.

No lender can guarantee approval regardless of credit history. Any lender claiming guaranteed approval without reviewing financials is a red flag and likely predatory.

On-time payments for 6–12 months are typically reported to business credit bureaus and meaningfully improve your credit profile, opening access to lower-cost capital options.

At Fordham Capital, we've made the application process straightforward and reassuring. Dive in and explore your financial options with confidence, knowing there's no impact on your credit score and no obligations. We review your details and offer customized solutions based on what you're looking for.