Small business funding networks are systems that connect entrepreneurs to capital through structured intermediaries, lender collaborations, or community-driven platforms. Understanding how small business funding networks work is the first step toward choosing the right path for your business. The two most prominent models are the SBA’s loan guarantee network, anchored by the 7(a) loan program, and crowdfunding platforms that replace credit underwriting with community engagement. Fordhamcapital has helped businesses access over $120M in funding by navigating exactly these kinds of networks on behalf of clients.

A funding network is not a single lender. It is a structured system where intermediaries, guarantors, and platforms work together to move capital from sources to businesses. The SBA’s loan guarantee model is the clearest example of this in action.

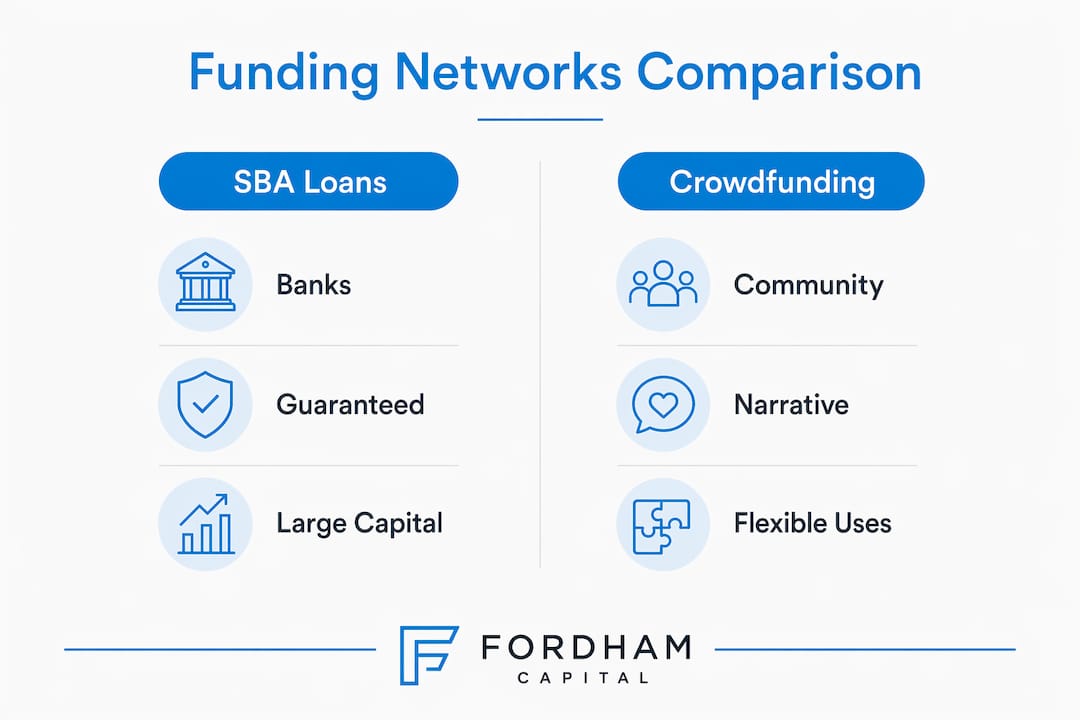

The SBA 7(a) program provides guarantees to authorized lenders, which reduces lender risk without the SBA itself providing loan funds. That distinction matters. The SBA is not writing you a check. It is standing behind the loan so that a bank or credit union feels safe enough to write one. This guarantee model forms the backbone of many small business financing options across the country.

The maximum loan amount under the SBA 7(a) program is $5 million, covering uses like working capital, equipment purchases, and real estate. Eligibility depends on your business’s income sources, credit history, and location. You repay the lender directly, not the SBA.

Pro Tip: Before you apply through any funding network, pull your business credit report and reconcile your financial statements. Lenders in every network will ask for these, and delays in gathering documents are the most common reason approvals stall.

SBA Lender Match is a structured referral tool, not a loan provider. You submit your business profile, and the system connects you with SBA-approved lenders who may be interested in your application. Each lender then runs its own underwriting process and sets its own documentation requirements.

This means two businesses with identical profiles can receive very different experiences depending on which lender they are matched with. Speed, required documents, and approval criteria all vary. Knowing this upfront saves you from assuming a match equals an approval.

Crowdfunding uses online platforms to raise capital from many people in small amounts, typically in exchange for rewards, equity, or future repayment. It is campaign-based rather than underwriting-based. Your credit score matters far less than your story and your audience.

There are four main crowdfunding types, each with different implications for your business:

Crowdfunding redefines funding networks by emphasizing narrative and community over financial history. This makes it a strong option for early-stage businesses that lack the credit profile required by traditional lenders.

Pro Tip: Treat your crowdfunding campaign like a product launch. Build your audience before you go live, not after. Email lists, social media followings, and community groups are your pre-launch fuel.

Crowdfunding platforms handle payment processing, but fundraising success depends on active campaign management and your network reach. The platform gives you infrastructure. You supply the momentum.

A crowdfunding campaign functions like a sales funnel with distinct stages: awareness, engagement, conversion, and follow-up. Businesses that treat each stage deliberately raise more. Those that post once and wait typically fall short of their goals.

The right funding network depends on your business profile, capital needs, and timeline. The table below compares the two primary models across the factors that matter most to small business owners.

| Factor | SBA loan network | Crowdfunding network |

|---|---|---|

| Capital source | Banks and credit unions with SBA guarantee | Individual backers or investors via platform |

| Underwriting basis | Credit history, financials, business plan | Campaign story, audience size, promotion quality |

| Maximum funding | Up to $5 million (SBA 7(a)) | Varies by platform and campaign goal |

| Timeline to funding | Weeks to months | Days to weeks after campaign closes |

| Equity retained | Full ownership retained | Partial ownership lost in equity crowdfunding |

| Best fit | Established businesses with credit history | Early-stage or consumer-facing businesses |

SBA loan networks suit businesses with documented financials and a need for larger capital amounts. Crowdfunding suits businesses with strong community ties or consumer products that benefit from public validation. Some businesses use both at different stages, which is a legitimate network funding strategy.

Hybrid models also exist. Community Development Financial Institutions, known as CDFIs, operate as mission-driven lenders that blend elements of both models. They often serve businesses in underserved markets that fall outside traditional bank criteria. For a broader view of your small business capital sources, comparing all available options before committing to one network saves time and money.

Preparation determines your outcome in any funding network. Disorganized documentation is the single most common reason small business owners lose momentum after a promising start.

Start with these fundamentals before approaching any network:

Once you submit through SBA Lender Match, follow up with matched lenders within 24 hours. Lenders work with multiple applicants simultaneously, and early responsiveness signals that you are a serious borrower. Delays on your end often result in lenders moving on.

For crowdfunding, the preparation shifts from financial documents to audience building. Your campaign’s success is driven by promotion timeline and audience engagement, not just the quality of your product. Reach out to local business groups, past customers, and industry contacts before your campaign goes live.

Pro Tip: Use your 2026 funding checklist to verify you have every document in order before submitting to any network. Missing one item can delay approval by weeks.

The most frequent mistake business owners make is approaching a funding network without knowing which type fits their situation. Applying to an SBA lender with a two-month-old business and no revenue history wastes time for everyone. Launching a crowdfunding campaign with no existing audience produces the same result.

Match your business profile to the network model before you invest time in applications. If your credit profile is thin, crowdfunding or CDFIs are more realistic starting points. If you have two or more years of documented revenue, SBA loan networks offer better terms and higher capital limits. Reviewing how to compare lender approval processes before you apply gives you a real advantage.

Small business funding networks work by matching entrepreneurs to capital through intermediaries, guarantors, or community platforms, and choosing the right model requires matching your business profile to the network’s criteria.

| Point | Details |

|---|---|

| SBA 7(a) is a guarantee network | The SBA reduces lender risk but does not provide funds directly; lenders underwrite and approve loans. |

| Crowdfunding replaces credit with community | Campaign success depends on story, audience size, and active promotion, not financial history. |

| Preparation drives outcomes | Organized financial documents and fast follow-up are the top factors in network funding success. |

| Network type must match business profile | Established businesses fit SBA loan networks; early-stage or consumer brands fit crowdfunding better. |

| Hybrid strategies are valid | Using SBA loans and crowdfunding at different growth stages is a recognized and effective approach. |

Most business owners I speak with assume a funding network is just a list of lenders. That misunderstanding costs them months. A network is a system with rules, relationships, and timing. The SBA’s Lender Match tool is a perfect example. It looks like a search engine, but it functions more like a warm introduction. How you show up after that introduction determines everything.

Crowdfunding gets underestimated in a different way. Business owners treat it as a last resort when traditional lenders say no. That is backwards. Crowdfunding works best when you have an engaged audience and a product people want to champion publicly. It is not a fallback. It is a different tool entirely.

The trend I see accelerating in 2026 is business owners using multiple networks in sequence. They use crowdfunding to validate a product and build a customer base, then use that traction as evidence when applying for an SBA loan. That sequence is smart. It turns community support into financial credibility.

The one thing I tell every business owner: do not wait until you need money to build relationships in funding networks. The owners who get funded fastest are the ones who started preparing six months before they needed capital. Reactive funding is expensive. Proactive preparation is free.

— Rob

Fordhamcapital works with small and medium-sized businesses that need capital fast and cannot afford to wait weeks for a traditional bank decision. With an A+ BBB rating and over $120M funded, Fordhamcapital connects business owners to a wide network of banks and lenders through a one-page application that does not impact your credit score.

Approvals come within 24 hours. That speed matters when a growth opportunity has a deadline. Whether you are exploring SBA-affiliated lenders or need a direct funding solution, Fordhamcapital’s team provides personalized guidance at every step. Apply now and find out what your business qualifies for today.

Small business funding networks are systems that connect entrepreneurs to capital through intermediaries such as the SBA, lender platforms, or crowdfunding sites. Each network type operates differently based on how it sources and distributes capital.

The SBA guarantees loans made by approved lenders, reducing lender risk without providing funds directly. Borrowers repay the lender, and the SBA 7(a) maximum is $5 million.

Crowdfunding raises capital from many individuals through online platforms, relying on campaign story and audience rather than credit underwriting. It is faster to launch but requires active promotion to succeed.

Crowdfunding and CDFIs are the most accessible options for startups without an established credit profile. SBA loan networks generally require documented revenue and credit history.

SBA loan networks typically take weeks to months depending on lender underwriting timelines. Crowdfunding campaigns can close and distribute funds within days to weeks after the campaign ends.

At Fordham Capital, we've made the application process straightforward and reassuring. Dive in and explore your financial options with confidence, knowing there's no impact on your credit score and no obligations. We review your details and offer customized solutions based on what you're looking for.