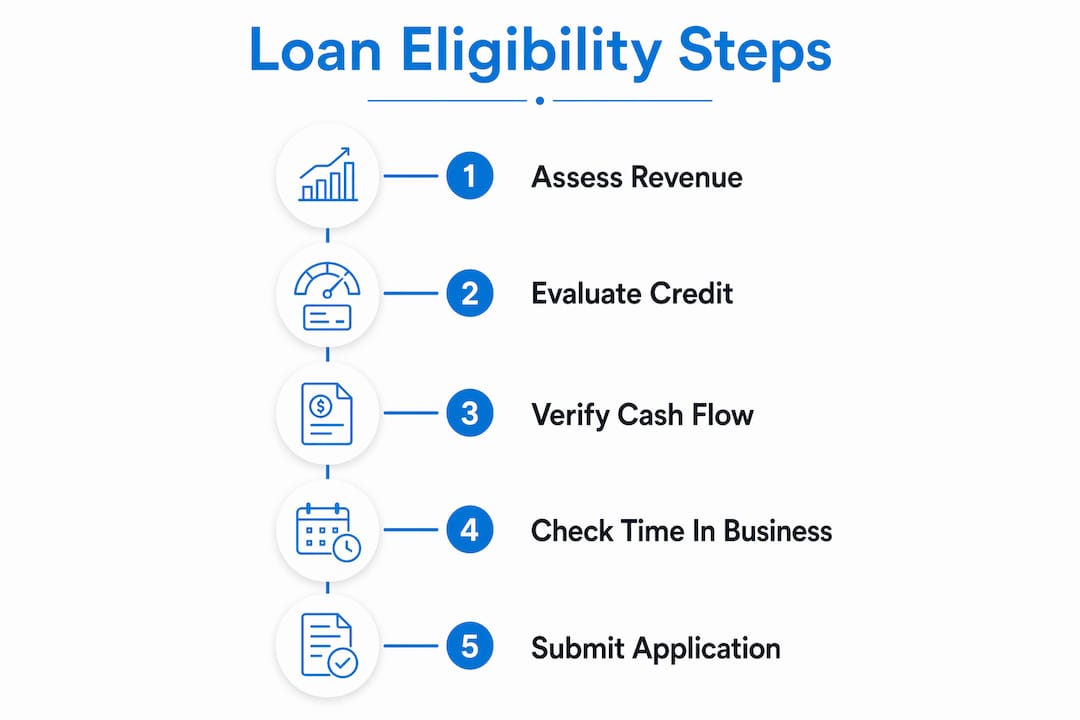

Business revenue is the single most important factor lenders use to determine loan eligibility. It tells lenders whether your company generates enough cash to repay what it borrows. Understanding how business revenue affects loan eligibility gives you a clear advantage before you ever fill out an application. The higher and more consistent your revenue, the more financing options open up, and the better the terms you can expect.

Lenders treat revenue as proof of repayment ability. Without sufficient revenue, even a strong credit score may not be enough to secure funding. Lenders need to see that your business earns enough money each month to cover its existing obligations and a new loan payment on top of them. Revenue is not just a number. It is the foundation of every loan decision a lender makes.

Minimum monthly revenue requirements typically start at $5,000 to $10,000 for specialized products like revenue-based financing or merchant cash advances. That threshold reflects the minimum cash flow a lender considers viable for repayment. Traditional banks set the bar much higher. They often require at least $250,000 in annual revenue before they will consider a business for a secured loan product. That gap between alternative lenders and banks is where most small business owners find themselves navigating their options.

Revenue requirements vary significantly by lender type and loan product. Knowing the specific threshold before you apply saves time and protects your credit profile.

| Loan Type | Lender Category | Typical Revenue Requirement |

|---|---|---|

| Merchant cash advance | Alternative lender | $5,000+ per month |

| Revenue-based financing | Alternative lender | $5,000–$10,000 per month |

| Online term loan | Online lender | $10,000–$15,000 per month |

| SBA loan | Bank or credit union | $250,000+ per year |

| Secured bank loan | Traditional bank | $250,000+ per year |

Online lenders tend to have more lenient revenue requirements and faster approval processes than traditional banks. That makes them a practical starting point for businesses that are still building their revenue track record. Banks, by contrast, require significant revenue and credit history before they will approve a loan application. The table above reflects general market ranges. Individual lenders set their own thresholds, so always confirm the specific requirement before applying.

Pro Tip: Check the lender’s minimum revenue requirement on their website or by calling directly before submitting any application. Applying below the threshold wastes time and can trigger a hard credit inquiry.

Raw revenue totals only tell part of the story. Lenders dig deeper into the quality and consistency of that revenue before making a decision.

The most important metric lenders calculate is the debt service coverage ratio, or DSCR. DSCR equals annual operating income divided by annual debt payments. A DSCR of 1.5 means your business earns 1.5 times its total debt obligations, which signals strong repayment ability. Lenders typically require a DSCR above 1.25 to approve a loan. Falling below that threshold tells the lender your business may struggle to cover payments if revenue dips even slightly.

Beyond DSCR, lenders look at these revenue quality factors:

A business earning $15,000 per month with steady deposits and a DSCR of 1.4 will often outperform a business earning $25,000 per month with erratic cash flow and a DSCR of 1.1. Lenders price risk, and consistency reduces risk.

Your current revenue level does not just affect whether you qualify. It determines which financing products are even available to you.

Businesses with low or inconsistent revenue usually rely on alternative financing such as invoice factoring or revenue-based loans. Higher revenue businesses qualify for traditional loans with better terms, lower interest rates, and longer repayment periods. The financing path you take is largely determined by where your revenue sits right now.

Here is how to match your financing type to your current revenue level:

Banks generally require good to excellent credit scores of 690 or above, strong finances, and at least two years in business. Many SBA lenders share that two-year requirement, while online lenders often accept businesses with as little as six months of operating history. Revenue level and business age work together. A newer business with strong revenue can sometimes offset the age requirement with online lenders.

Improving your revenue picture before applying is the most direct way to maximize loan approval odds. Most lenders look at the last 3–6 months of bank statements, so the work you do now shows up quickly.

A thorough business plan can help businesses with insufficient revenue by demonstrating future earnings potential. Documentation proving the ability to cover loan payments increases lender confidence and approval likelihood. If your revenue is currently low or seasonal, a well-structured business plan with realistic projections gives lenders a reason to look past the current numbers. Read more about the role of a business plan in the loan approval process.

Pro Tip: Reduce your DSCR risk before applying by paying down any existing short-term debt. Even eliminating one small monthly obligation can push your ratio above the 1.25 threshold lenders require.

Best practices for improving your revenue visibility before applying:

Common reasons for business loan denial include insufficient revenue, weak cash flow, and short time in business. Each of these is addressable with the right preparation. Understanding why applications get rejected is the first step toward avoiding those mistakes.

| Rejection Reason | What It Signals to Lenders | How to Address It |

|---|---|---|

| Revenue below minimum threshold | Business cannot cover loan payments | Build revenue for 3–6 months before reapplying |

| Inconsistent cash flow | High repayment risk | Stabilize monthly deposits and reduce expense volatility |

| DSCR below 1.25 | Existing debt leaves little room for new payments | Pay down current obligations before applying |

| Less than 6–12 months in business | Insufficient revenue track record | Use alternative lenders with lower time requirements |

| Revenue and tax return mismatch | Credibility concern | Reconcile all financial records before submitting |

The most common mistake small business owners make is applying too early. Waiting an extra quarter to build a stronger revenue track record often results in better loan terms, not just a higher approval chance. Lenders reward patience with lower rates. Read more about why banks reject small business loans and how to get ahead of those issues.

Business revenue directly determines both your loan eligibility and the financing products available to you, with lenders requiring consistent cash flow, a DSCR above 1.25, and revenue that aligns across all financial documents.

| Point | Details |

|---|---|

| Revenue sets the baseline | Lenders use revenue to confirm your business can cover loan payments each month. |

| DSCR is the key ratio | A DSCR above 1.25 signals repayment ability; below that, most lenders will decline. |

| Revenue level shapes your options | Higher monthly revenue unlocks traditional bank loans with lower rates and longer terms. |

| Consistency matters as much as size | Steady monthly deposits reduce lender risk and strengthen your application. |

| Preparation closes the gap | Reconciled records, separated finances, and a business plan improve approval chances significantly. |

Most small business owners walk into a loan application focused on the total number. They think if their annual revenue looks big enough, the approval will follow. That is not how lenders actually think.

What I have seen repeatedly is that lenders care more about the story your revenue tells than the headline figure. A business earning $180,000 a year with perfectly consistent monthly deposits and a clean DSCR will beat a business earning $300,000 a year with erratic cash flow and three months of low deposits right before the application. Lenders are not just checking a box. They are trying to predict your behavior as a borrower.

The other thing most owners underestimate is documentation. Lenders do not take your word for anything. They want bank statements, tax returns, and profit and loss statements that all point to the same conclusion. When those documents conflict, the application stalls or gets denied. I have seen strong businesses lose funding because their bookkeeper was six months behind on reconciliations.

My honest advice: treat your loan application as a presentation, not a form. The revenue data you submit is your argument. Build it deliberately, clean it up before you apply, and make sure every document reinforces the same narrative. That preparation is what separates approvals from rejections.

— Rob

Revenue requirements should not lock you out of the funding your business needs to grow. Fordhamcapital works with small and medium-sized businesses across a wide range of revenue profiles, connecting owners to a network of banks and lenders through a one-page application with no credit impact.

Fordhamcapital has funded over $120M and helped clients generate more than $500M in revenue, backed by an A+ BBB rating. Approvals happen within 24 hours. Whether your revenue is growing, seasonal, or still building, you can start your application today and find out which financing options match your current profile.

Minimum monthly revenue starts at $5,000 to $10,000 for alternative products like merchant cash advances, while traditional banks typically require $250,000 or more in annual revenue.

DSCR stands for debt service coverage ratio and measures your operating income against your debt payments. Lenders typically require a DSCR above 1.25, meaning your business earns at least 1.25 times what it owes in annual debt obligations.

Yes, but your options narrow. Businesses with variable revenue often qualify for revenue-based financing or invoice factoring, which are products designed to flex with your cash flow rather than require fixed monthly payments.

Most lenders review 3–6 months of bank statements, while traditional banks and SBA lenders often want 2 years of tax returns and financial records to assess long-term revenue stability.

Mixing personal and business finances makes it harder for lenders to calculate your true business revenue and DSCR. Separate accounts give lenders a clean picture and remove a common reason for delays or denials.

At Fordham Capital, we've made the application process straightforward and reassuring. Dive in and explore your financial options with confidence, knowing there's no impact on your credit score and no obligations. We review your details and offer customized solutions based on what you're looking for.