Funding small business expansion quickly means getting capital into your hands fast enough to act on growth before the moment passes. 46% of small businesses sought financing specifically to pursue expansion or new opportunities. That number tells you something real: growth windows close fast, and slow capital kills deals. The right fast business funding options, from invoice factoring to merchant cash advances to SBA loans, can put you in position to hire, expand inventory, or open a new location without waiting months for a traditional bank decision.

The fastest path to capital depends on your business model, revenue type, and how quickly you need funds. Each option below carries different speeds, costs, and qualification requirements. Understanding the differences before you apply saves you time and protects your cash flow.

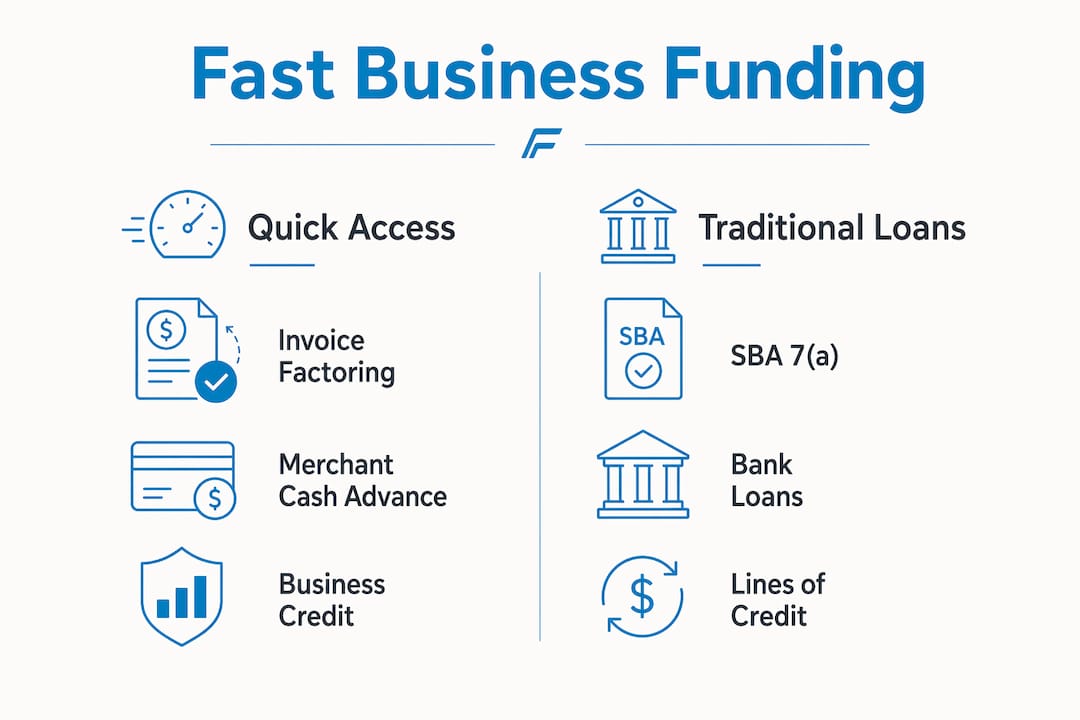

Invoice factoring is not a loan. It is a sale of your outstanding invoices to a factoring company, which keeps debt off your balance sheet and focuses approval on your customers’ creditworthiness rather than yours. Invoice factoring advances 70–95% of invoice value within 24–48 hours. That speed makes it one of the strongest fast business funding options for B2B companies with reliable receivables. The remaining balance arrives after your customer pays, minus the factoring fee.

Merchant cash advances (MCAs) provide a lump sum in exchange for a percentage of future sales. Approvals often happen within 24 hours, and funds land within 1–3 business days. The catch is cost. MCA effective costs rise sharply with faster repayment, so you need to model your daily remittance against your sales volume before signing. A business with volatile revenue can find itself squeezed during the same expansion it funded.

SBA 7(a) loans offer lower interest rates and longer repayment terms, but they move slower. Standard SBA loans can take 30–90 days. The SBA now requires a debt service coverage ratio of 1.1:1 for 7(a) Small Loans under revised March 2026 underwriting standards. That means your business must generate at least $1.10 in net operating income for every $1.00 of debt payment. SBA loans reward preparation, not speed.

Business lines of credit give you revolving access to capital you draw as needed. They work well for expansion phases where costs arrive in stages, such as phased hiring or rolling inventory purchases. Microloans, offered through nonprofits and SBA intermediaries, cap out around $50,000 but carry lower credit thresholds and suit early-stage businesses.

| Funding Type | Typical Speed | Amounts | Credit Requirement | Relative Cost |

|---|---|---|---|---|

| Invoice Factoring | 24–48 hours | $5,000–$5M+ | Customer credit matters most | Moderate |

| Merchant Cash Advance | 1–3 days | $5,000–$500,000 | Low to moderate | High |

| SBA 7(a) Loan | 30–90 days | Up to $5M | Moderate to strong | Low |

| Business Line of Credit | 3–14 days | $10,000–$500,000 | Moderate | Low to moderate |

| Microloan | 1–4 weeks | Up to $50,000 | Low | Low to moderate |

Pro Tip: Match your funding type to your revenue model. If you invoice other businesses, factoring is your fastest path. If you run a retail or restaurant operation with daily card sales, an MCA gives you speed. If you can wait 30 days and want the lowest cost, pursue an SBA loan.

Small banks report higher full approval rates for small business applicants than large banks or online fintech lenders. That does not mean fintech is wrong for you. It means you should apply to multiple sources simultaneously rather than betting on one.

Document preparation is where most fast funding applications either accelerate or stall. Lenders do not slow down because they are disorganized. They slow down because your paperwork forces them to ask questions.

Lenders typically require 6–12 months of business bank statements, two years of business tax returns, and year-to-date financials dated within 60–90 days. Gather these before you apply, not after. Every day you spend collecting documents after submission is a day added to your approval timeline.

Here is what a lender-ready packet looks like:

Accuracy matters as much as completeness. Mismatches between claimed financials and lender verification are one of the top causes of underwriting delays. If your bank deposits do not match your reported revenue, expect a re-request. Reconcile your bookkeeping monthly so your bank statements, profit and loss, and tax returns all tell the same story.

Pro Tip: Place a one-page summary at the top of your document package. Include your business name, funding amount requested, use of funds, monthly revenue, and time in business. Organizing a one-page summary helps underwriters understand your request immediately, which cuts review time. See the 2026 funding checklist for a complete document list by funding type.

For SBA loans specifically, you will also need a personal financial statement (SBA Form 413), a statement of personal history (SBA Form 912), and a detailed business plan. SBA documentation requirements are heavier than most alternative lenders, which is the tradeoff for lower rates.

Speed in funding comes from process discipline, not luck. Follow these steps in order and you cut days off your timeline.

| Funding Type | Typical Application to Funding Timeline |

|---|---|

| Invoice Factoring | 24–48 hours |

| Merchant Cash Advance | 1–3 business days |

| Business Line of Credit | 3–14 business days |

| Microloan | 1–4 weeks |

| SBA 7(a) Loan | 30–90 days |

If your credit history is limited or imperfect, focus on factoring and MCAs first. Both products prioritize revenue and customer quality over personal credit scores. You can also explore funding options with low credit scores that are specifically structured for businesses in your position.

Most funding delays are preventable. The problems below appear repeatedly across applications and cost business owners days or weeks they cannot afford.

Document mismatches are the single most common delay. If your tax return shows $400,000 in revenue but your bank deposits show $320,000, the lender will stop and ask questions. Reconcile every number before you submit.

Unclear use of funds raises red flags. Lenders want to know that the capital produces a return. “Working capital” is not a use of funds. “Hiring two additional technicians to fulfill $180,000 in contracted work” is a use of funds.

Underestimating repayment burden creates cash flow problems mid-expansion. Factoring costs depend heavily on customer credit and invoice terms, so a portfolio of slow-paying clients raises your effective cost. Model your repayment against your worst-case revenue month, not your best.

Here are the most common obstacles and how to address them:

Transparent communication with your lender also matters. If your financials show a down quarter, explain it proactively. Lenders respond better to context than to silence. A brief note explaining a seasonal dip or a one-time expense shows professionalism and reduces underwriting friction.

Funding small business expansion quickly requires matching the right financing type to your business model, preparing complete and consistent documents before applying, and managing lender communication actively throughout the process.

| Point | Details |

|---|---|

| Match funding to your model | Invoice factoring suits B2B firms; MCAs work for retail and restaurant businesses with daily card sales. |

| Prepare documents before applying | Assemble bank statements, tax returns, and year-to-date financials before your first submission to avoid delays. |

| Apply to multiple sources | Submitting to a fintech lender, small bank, and specialty lender simultaneously gives you options and speeds decisions. |

| Reconcile financials monthly | Mismatches between bank deposits and reported revenue are the top cause of underwriting slowdowns. |

| Model MCA repayment carefully | Calculate your daily remittance against your lowest-revenue month before signing a merchant cash advance. |

The business owners who secure capital fastest are not the ones with the best credit. They are the ones who treat their financial documents like a product they are selling. Every number tells a story, and lenders are reading it whether you curate it or not.

The shift toward fintech and alternative lenders has genuinely changed the game for small businesses. Five years ago, a business with 18 months of operating history and a 620 credit score had almost no options. Today, that same business can access invoice factoring, an MCA, or a specialty lender within 72 hours. The options are real. The risk is that speed creates pressure to skip the analysis.

The mistake I see most often is treating the funding decision as a finish line. Signing a term sheet is not the goal. Deploying capital that generates more than it costs is the goal. Before you sign anything, calculate the total repayment amount and divide it by your projected monthly revenue. If repayment consumes more than 15–20% of monthly revenue, you are taking on real cash flow risk during the exact period you need flexibility.

My honest advice: build your document packet now, before you need funding. Reconcile your books monthly. Keep your bank statements clean. When the growth opportunity arrives, you will be ready to move in 48 hours instead of two weeks. That preparation is a competitive advantage most of your competitors do not have.

— Rob

Fordhamcapital was built for exactly the situation you are in: a growth opportunity in front of you and a traditional bank that moves too slowly to help.

Fordhamcapital’s one-page application connects you to a wide network of banks and lenders, with approvals possible within 24 hours and no credit impact from the inquiry. With over $120M funded and clients generating more than $500M in revenue, Fordhamcapital has the track record to back its process. The A+ BBB rating reflects a commitment to transparency that most fast lenders cannot match. If you are ready to secure fast business funding and stop waiting on a bank that was never built for your business, Fordhamcapital is the place to start.

Invoice factoring and merchant cash advances are the fastest options, with funds available in 24–48 hours and 1–3 business days respectively. Both prioritize revenue over credit scores, making them accessible to most small businesses.

Requirements vary by product, but most alternative lenders look for at least $10,000 in monthly revenue and 6 or more months in business. Invoice factoring focuses on your customers’ creditworthiness rather than your own.

Many alternative lenders and specialty funders, including Fordhamcapital, use soft inquiries that do not impact your credit score. Confirm the inquiry type before submitting any application.

Lenders typically require 6–12 months of bank statements, two years of tax returns, and year-to-date financials. Having these ready before you apply is the single fastest way to cut your approval timeline.

Yes. Invoice factoring, merchant cash advances, and several low-documentation loan products are available to business owners with limited or imperfect credit histories. Approval depends more on revenue consistency and customer quality than on your personal credit score.

At Fordham Capital, we've made the application process straightforward and reassuring. Dive in and explore your financial options with confidence, knowing there's no impact on your credit score and no obligations. We review your details and offer customized solutions based on what you're looking for.