A low documentation business loan is a financing product that replaces full tax returns and audited financial statements with alternative income evidence, such as 6 to 12 months of business bank statements or BAS statements. This makes it one of the most accessible funding paths for small business owners, sole traders, and entrepreneurs whose financial records don’t fit the traditional bank mold. The industry standard term is “low-doc loan,” and understanding exactly what it requires, what it costs, and who qualifies separates smart borrowers from those who pay too much or get declined unnecessarily.

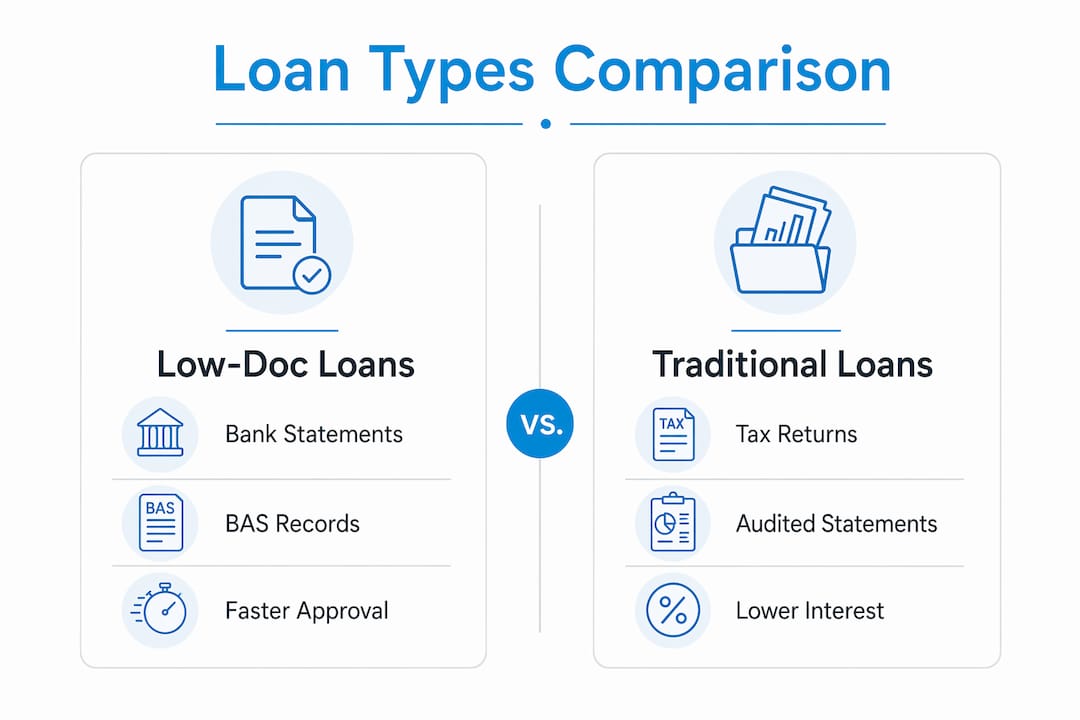

A low-doc loan, as the industry calls it, uses alternative income evidence such as bank statements or BAS statements instead of the full tax returns and financial reports that conventional lenders demand. This matters because millions of small businesses operate profitably without clean, multi-year tax histories. Seasonal businesses, newer startups, and sole traders with mixed personal and business income all fall into this category.

The core mechanic is straightforward. Instead of proving income through an accountant-prepared profit and loss statement, you demonstrate it through your actual banking behavior. Lenders look at cash flow patterns, deposit consistency, and how you manage debts. The result is a faster, leaner process that gets capital into your hands without the months-long documentation chase that traditional bank loans require.

Low-doc loans are not the same as no-doc loans, and that distinction matters financially. Low-doc still requires some verified income evidence. No-doc relies entirely on asset security. Confusing the two leads borrowers to either over-prepare or under-prepare, both of which cost time and money.

The phrase “low paperwork business loans” can mislead people into thinking almost nothing is needed. In practice, lenders request a specific, manageable set of documents that verify your business exists and generates real income.

The standard documentation package includes:

Loan terms range from 3 months to 5 years depending on the lender and whether the loan is secured or unsecured. That range reflects the flexibility low-doc products offer compared to the rigid structures of conventional bank financing.

One detail most borrowers miss: the combination of documents you submit directly affects your interest rate. Combining BAS with bank statements typically secures more competitive rates than submitting bank statements alone. Submitting only bank statements is faster but usually carries a higher rate because the lender has less verified data to work with.

Pro Tip: Gather your last 12 months of bank statements and your four most recent BAS statements before you apply. Having both ready from day one puts you in the stronger documentation tier and can meaningfully reduce your interest rate.

Eligibility for low-doc business funding is broader than most people expect, but it is not unlimited. Lenders apply a clear set of criteria that balance accessibility with risk management.

The typical qualification checklist in 2026 looks like this:

Sole traders, SMEs with seasonal revenue, and businesses with impaired credit can all qualify. If your credit history has blemishes, you can explore business funding with low credit scores as a parallel path. The trade-off is that impaired credit typically results in a higher interest rate, not an automatic rejection.

Banking conduct weighs more heavily than single monthly revenue figures in loan underwriting. A business generating $30,000 per month with consistent deposits and no dishonors will often outperform a business generating $50,000 per month with irregular patterns and frequent overdrafts.

Pro Tip: In the 90 days before you apply, treat your business bank account like it’s already being audited. Avoid overdrafts, clear any small outstanding debts, and keep your deposit patterns consistent. That 90-day window is what lenders scrutinize most.

The trade-offs in low-doc lending are real and worth understanding clearly before you commit.

| Feature | Low-doc loans | Traditional bank loans |

|---|---|---|

| Interest rate (first mortgage) | 9.50% to 13.95% p.a. | 6% to 9% p.a. (typical) |

| Interest rate (second mortgage) | 1.20% to 1.95% monthly | Rarely available |

| Loan size range | $5,000 to $5 million | $10,000 to $5 million+ |

| Approval time (unsecured) | 24 to 48 hours | 2 to 6 weeks |

| Approval time (property-backed) | 7 to 14 business days | 4 to 8 weeks |

| Documentation required | Bank statements, BAS, ID | Full tax returns, financials, business plans |

Interest rates range from 9.50% to 13.95% p.a. for first mortgage structures, and 1.20% to 1.95% monthly for second mortgage products. That premium over conventional bank rates exists because lenders are accepting more risk by verifying less. The rate is the price of speed and accessibility.

Loan sizes range from $5,000 up to $5 million for property-backed facilities, with unsecured options typically capping lower. For most small businesses, the $50,000 to $500,000 range covers the majority of real operational needs, from equipment purchases to inventory builds to bridging seasonal cash flow gaps.

The approval speed advantage is where low-doc products genuinely outperform. Online lenders can fund within 24 to 48 hours for unsecured applications. That speed is not possible with conventional bank loans, which require committee reviews, full credit assessments, and multi-week processing cycles. For a business owner facing a time-sensitive opportunity, that difference is decisive.

Low-doc loans exist to bridge financing gaps for profitable businesses that lack extensive historical financial records. The practical applications are wide, and understanding where these loans perform best helps you deploy capital effectively.

Common use cases where low-doc business funding delivers real value:

The drawbacks are equally worth naming. Interest rates are higher than conventional loans. Some unsecured products carry shorter repayment terms, which increases monthly payment pressure. And if your business banking conduct is poor, the very documents you submit become evidence against you rather than for you.

The clearest benefit is access. For businesses that cannot satisfy traditional bank requirements, low-doc loans are not a compromise. They are often the only viable path to growth capital.

These three loan categories serve different borrower profiles, and choosing the wrong one wastes time and money.

| Loan type | Income documentation | Typical cost | Best for |

|---|---|---|---|

| Conventional full-doc | Full tax returns, audited financials | Lowest rates | Established businesses with clean records |

| Low-doc | Bank statements, BAS, income declaration | Moderate premium | SMEs, sole traders, seasonal businesses |

| No-doc | None (asset security and exit strategy only) | Highest rates | Asset-rich businesses with no income records |

No-doc loans require zero income documentation and rely on asset security and a clear exit strategy. They are not “no assessment” products. Lenders still verify business existence, conduct asset valuations, and require a credible repayment plan. No-doc loans are generally more expensive because the lender carries significantly more risk.

Choosing between low-doc and no-doc depends entirely on your documentation readiness and asset position. If you have six months of clean bank statements and recent BAS records, low-doc is almost always the better choice. It costs less and is more widely available. Applying for no-doc without adequate asset security or a clear exit plan risks refusal or rates that make the loan economically unviable.

Conventional full-doc loans remain the cheapest option when you qualify. If your business has two or more years of clean tax returns and stable revenue, pursuing a traditional bank loan is worth the wait. The rate savings over a $500,000 facility can be substantial over a three to five year term.

Pro Tip: Before applying for any loan product, honestly assess which documentation tier you can satisfy. Applying for a low-doc loan when you actually qualify for full-doc costs you money. Applying for no-doc when you have adequate income records costs you even more.

Low-doc loans are the most practical funding path for small businesses that generate real income but cannot satisfy traditional bank documentation requirements.

| Point | Details |

|---|---|

| Definition of low-doc loans | These loans use bank statements and BAS records instead of full tax returns to verify income. |

| Documentation still required | Expect to provide 6 to 12 months of bank statements, BAS, ID, and proof of business registration. |

| Eligibility threshold | A minimum credit score around 400 and an active ABN for 6 months are the baseline requirements. |

| Cost vs. speed trade-off | Rates run 9.50% to 13.95% p.a. for secured products, with approvals possible within 24 to 48 hours. |

| Banking conduct matters most | Consistent deposits and no dishonored payments carry more weight than raw revenue figures. |

I’ve seen a consistent pattern with business owners who approach low-doc lending for the first time. They either assume it means almost no scrutiny, or they over-prepare and submit documents that actually hurt their application by revealing inconsistencies they hadn’t noticed.

The real insight is this: low-doc lending is not about hiding your financial situation. It’s about presenting it through a different lens. Your bank statements are a live record of how you actually run your business. Lenders read them the way an experienced accountant reads a balance sheet. They see the patterns, the timing of deposits, the frequency of withdrawals, and the moments where cash got tight.

What I tell every business owner I work with is to spend 30 days cleaning up their banking behavior before they apply. Not manipulating it. Cleaning it. Pay down small outstanding balances. Stop using the business account for personal expenses. Make sure every deposit has a clear, traceable source. That preparation alone can move you from a borderline approval to a confident one, and from a higher rate tier to a lower one.

The other mistake I see constantly is applying for the wrong product. Someone with solid bank statements and recent BAS records applies for a no-doc loan because they heard it was “easier.” It isn’t. It’s more expensive and harder to get approved for without strong asset security. If you have the documentation for a low-doc loan, use it. The rate difference over a 24-month term on a $200,000 facility is not trivial.

If you want to understand how high-risk loan criteria compare to low-doc eligibility, that context helps you position your application correctly from the start.

— Rob

Fordham Capital specializes in exactly the kind of funding this article describes: fast, flexible, and built for businesses that traditional banks overlook.

The application process at Fordham Capital starts with a single page, avoids any credit impact during the inquiry stage, and connects you to a wide network of lenders within 24 hours. With an A+ BBB rating and over $120M funded, Fordham Capital has helped clients generate more than $500M in revenue by getting capital to them when they needed it. If you’re ready to explore fast, flexible business funding without the paperwork burden of a traditional bank loan, Fordham Capital is the place to start.

A low-doc business loan replaces full tax returns with alternative income evidence like bank statements and BAS records. It gives businesses with limited financial history faster access to capital with less paperwork.

Loan sizes range from $5,000 to $5 million depending on whether the loan is secured by property or unsecured. Most small business applications fall in the $50,000 to $500,000 range.

Online lenders can approve and fund unsecured low-doc loans within 24 to 48 hours. Property-backed applications typically take 7 to 14 business days to settle.

The minimum credit score is around 400 for most low-doc lenders, which is significantly lower than the thresholds traditional banks apply. Impaired credit is sometimes accepted but results in a higher interest rate.

A low-doc loan requires some income evidence such as bank statements or BAS records. A no-doc loan requires none and relies entirely on asset security and a clear exit strategy, making it more expensive and harder to qualify for without strong collateral.

At Fordham Capital, we've made the application process straightforward and reassuring. Dive in and explore your financial options with confidence, knowing there's no impact on your credit score and no obligations. We review your details and offer customized solutions based on what you're looking for.