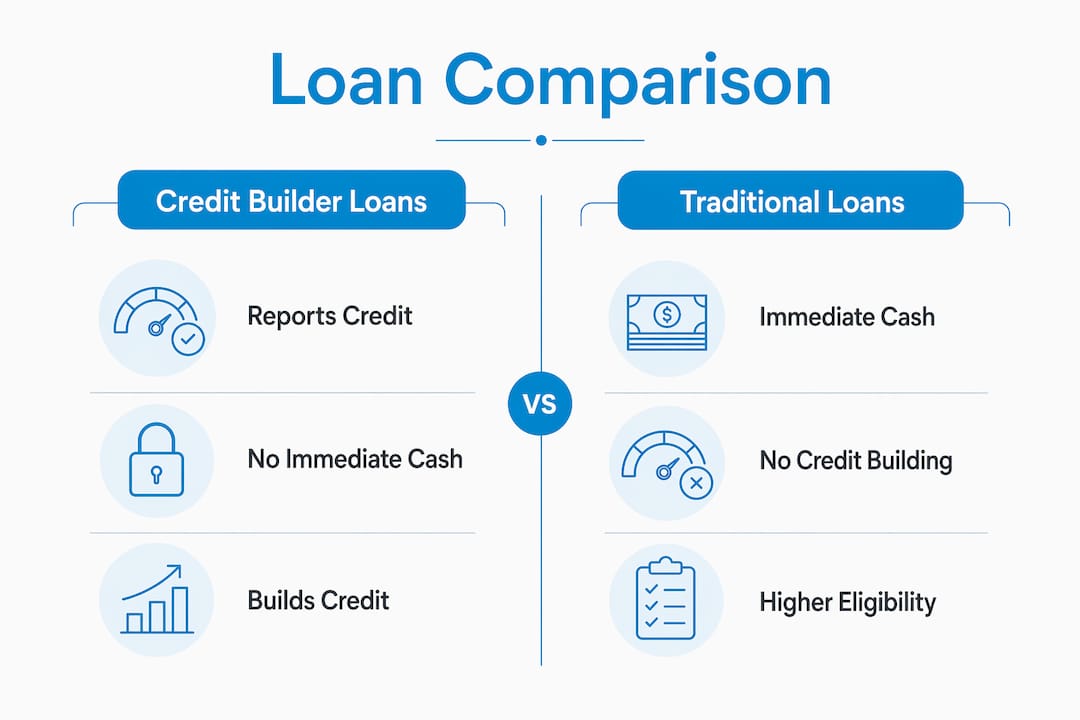

A credit builder business loan is a specialized financial product designed to help small businesses establish or strengthen their business credit profiles through scheduled payments reported to major credit bureaus. Unlike a traditional loan, it does not deliver immediate cash. Instead, it builds the credit foundation your business needs to qualify for larger funding later. Credit bureaus like Dun & Bradstreet, Experian, and Equifax track these payments and update your business credit profile accordingly. For startups and small businesses with thin or no credit history, this product is often the fastest legitimate path to creditworthiness.

A credit builder business loan works by holding your loan funds in a savings account or certificate of deposit while you make monthly payments. You do not receive the money upfront. The lender holds funds in a savings account secured by the loan until you complete the payment term or pay off the balance. Once the term ends, you receive the funds. The real value is not the money itself. It is the payment history that gets reported to business credit bureaus.

Each on-time payment builds a positive tradeline on your business credit report. A tradeline is simply a record of a credit account and its payment history. Lenders and vendors use these records to evaluate your business before extending credit or approving loans.

Business credit profiles typically reflect new tradelines within 30–60 days if payments are consistent. That timeline means a disciplined business owner can see measurable credit profile changes within two months of starting a credit builder program.

Pro Tip: Set up automatic payments the day you open a credit builder account. One missed payment can erase weeks of positive reporting and set your credit building timeline back significantly.

Traditional small business loan options like SBA loans or term loans deposit funds directly into your account for immediate use. Credit builder loans do the opposite. The funds are locked away, and the payment discipline is the product. This distinction matters because many business owners apply for credit builder loans expecting working capital. They are credit tools, not cash solutions.

Credit building loans for businesses come in several forms. Each product reports differently and serves a different stage of credit development.

| Product | Reports to bureaus | Immediate cash | Best for |

|---|---|---|---|

| Credit builder savings loan | Dun & Bradstreet, Experian, Equifax | No | Zero-history startups |

| Secured business credit card | Experian, Equifax | Yes (credit line) | Building revolving history |

| Net-30 vendor account | Dun & Bradstreet | No | Early-stage tradelines |

| Installment credit builder loan | Varies by lender | No | Structured payment history |

Business credit builder products vary widely, so the best fit depends on your credit goals and current operational needs. A startup with no credit history benefits most from net-30 vendor accounts combined with a credit builder savings loan. A business with one year of history may get more value from a secured business card.

Pro Tip: Open at least two different types of credit builder products simultaneously. Lenders prefer seeing diverse tradelines over a single account, and the combined reporting accelerates your credit profile development.

Getting the mechanics right matters as much as choosing the right product. These steps give you the strongest foundation for building business credit.

Separate your business and personal credit legally. Register as an LLC and obtain an EIN from the IRS. Without this separation, your business cannot build its own credit identity. Personal credit and business credit are tracked by different bureaus using different scoring models.

Confirm your lender reports to all three major bureaus. Not all lenders report to Dun & Bradstreet, Experian, and Equifax. A lender that only reports to one bureau limits your credit profile growth. Always ask before you apply.

Keep credit utilization under 30%. Maintaining a utilization ratio under 30% is one of the most effective ways to maximize your credit score gains. If your secured card has a $1,000 limit, keep your balance below $300 at all times.

Combine multiple tradelines. Diversified tradelines create a stronger credit profile than relying on a single product. Pair a credit builder loan with a net-30 vendor account and a secured business card for the fastest results.

Monitor your business credit reports regularly. Check your Dun & Bradstreet, Experian Business, and Equifax Business reports at least quarterly. Errors on business credit reports are more common than most owners realize, and they go uncorrected unless you dispute them.

Pay every account on time, every month. This sounds obvious, but the discipline required is real. Late payments on credit builder accounts can negatively impact your scores and undo months of progress. Automate every payment.

Understanding how to improve your business credit score goes beyond just opening accounts. The combination of consistent payments, low utilization, and diverse tradelines is what moves the needle.

Credit builder loans offer real advantages for small businesses that use them correctly.

Benefits:

Limitations:

“Credit builder loans are for building creditworthiness, not survival cash. Entrepreneurs who treat them as emergency funding miss the point and often end up worse off.” — Nav, How to establish business credit

The most common misunderstanding is that credit builder loans are immediate cash solutions. They are not. They are long-term credit tools that pay off when you apply for a real loan six or twelve months later and qualify for better terms because of the work you did upfront.

A credit builder business loan builds your business credit profile through reported payments, not through immediate cash, making it a foundational tool for long-term funding access.

| Point | Details |

|---|---|

| Definition | A credit builder loan holds funds while you make payments reported to business credit bureaus. |

| Timeline | Business credit profiles reflect new tradelines within 30–60 days of consistent payments. |

| Legal separation | Register as an LLC and get an EIN before opening any credit builder account. |

| Diversify tradelines | Combine a credit builder loan, secured card, and net-30 accounts for the strongest profile. |

| Know the limits | Credit builder loans build credit only. They do not provide working capital or solve cash flow problems. |

Most small business owners I talk to discover credit builder loans too late. They apply for a $200,000 term loan, get declined because their business has no credit history, and then scramble to fix it. The smarter move is to start building business credit the day you register your LLC, not the day you need funding.

The other mistake I see constantly is treating credit builder products as a one-and-done solution. One net-30 account with Uline is not a credit profile. It is a starting point. The businesses that qualify for serious capital 12 months later are the ones that opened three or four tradelines, kept utilization low, and never missed a payment. That combination is what lenders actually want to see.

Credit builder loans also protect something most owners do not think about until it is too late: their personal credit. Business credit products report to business bureaus only, which means your personal score stays clean while your business builds its own identity. That separation is worth more than people realize when you eventually apply for a mortgage or personal line of credit.

My honest advice: start with a net-30 vendor account, add a secured business card, and open a credit builder savings loan all within the same 30-day window. Monitor your Dun & Bradstreet report monthly. Be patient. The businesses that do this consistently are the ones that come back to lenders like Fordhamcapital six months later with a real credit profile and get approved.

— Rob

Building business credit is the foundation. Accessing real capital is the goal.

Fordhamcapital has funded over $120M for small and medium-sized businesses, helping clients generate more than $500M in revenue. With an A+ BBB rating and a one-page application, Fordhamcapital connects you to a wide network of banks and lenders with approvals in as little as 24 hours. Once your credit profile is in shape, or even if you need funding options with low credit right now, Fordhamcapital has options built for businesses that traditional banks overlook. Apply today and find out what your business qualifies for.

A traditional business loan deposits funds directly into your account for immediate use. A credit builder loan holds the funds in a savings account while you make payments, building your credit profile through reported payment history.

Business credit profiles typically reflect new tradelines within 30–60 days of consistent, on-time payments. Significant credit profile improvement usually takes 6–12 months of disciplined use across multiple tradelines.

No. Business credit builder accounts report to business credit bureaus only, so your personal credit score is not impacted. This separation requires that your business is legally registered with its own EIN.

The most effective credit builder products report to Dun & Bradstreet, Experian Business, and Equifax Business. Always confirm reporting practices with a lender before applying, since not all providers report to all three bureaus.

Yes. Credit builder loans and net-30 vendor accounts are specifically designed for businesses with little or no credit history. Most do not require revenue verification, making them one of the most accessible small business loan options for early-stage companies.

At Fordham Capital, we've made the application process straightforward and reassuring. Dive in and explore your financial options with confidence, knowing there's no impact on your credit score and no obligations. We review your details and offer customized solutions based on what you're looking for.

.jpg)